by First Integrity Team Supreme Lending | Aug 30, 2024

An Overview of Supreme Lending Credit Score Requirements

When you’re preparing to buy a home, understanding the mortgage credit score requirements is essential. Your credit plays a significant role in determining your eligibility for various loan programs, as well as interest rates you may qualify for. Our goal at Supreme Lending is to provide the smoothest mortgage experience possible, that includes guiding you with transparent information to help you to make an informed, confident decision. Here’s an overview of Supreme Lending’s credit score requirements for common loan programs and frequently asked questions.

Conventional Loans

Conventional loans are popular among homebuyers due to their flexibility and competitive interest rates. As a general rule of thumb, Supreme Lending requires a minimum credit score of 620 for Conventional loans. However, a higher score typically results in securing more favorable rates and terms.

FHA Loans

Insured by the Federal Housing Administration, FHA loans are another common mortgage option –especially for first-time homebuyers or borrowers with lower credit. These loans have more lenient credit score requirements, accepting as low as 580.

VA Loans

For eligible military Veterans and active-duty personnel, VA loans offer affordable options as they don’t require a down payment or mortgage insurance premiums. Like FHA loans, Supreme Lending’s credit score requirement for VA loans is a minimum of 580.

USDA Loans

Guaranteed by the U.S. Department of Agriculture, USDA loans provide affordable financing designed for homebuyers in designated rural areas with no down payment required. In general, Supreme Lending’s credit score requirement for this program is 600.

Jumbo Loans

Jumbo loans are used to purchase high-value properties with a loan amount greater than conforming loan limits, which is $766,550 for one-unit homes in 2024. Due to potential higher lending risk, Jumbo loans typically have stricter qualifications. Supreme Lending has jumbo programs with a minimum credit score of 680, but depending on the loan guidelines, some may require at least a 720 credit score or higher.

Frequently Asked Questions

Now that you have a snapshot of common credit score requirements at Supreme Lending, here’s some more insight on how your credit can impact your mortgage.

How is a credit score determined?

A credit score, often represented by a FICO® score, is a numerical assessment of a borrower’s financial health. It is calculated based on several key factors:

- Payment History: Your record of on-time payments versus late or missed payments.

- Credit Utilization: The amount of credit you’re using compared to your total credit limits.

- Length of Credit History: The duration of time you’ve had credit accounts open.

- Types of Credit in Use. The variety of credit accounts you have, such as credit cards, mortgages, and car loans.

- Recent Credit Behavior. This includes how many new credit accounts you’ve opened recently and credit inquiries.

Combining these factors provides a numerical score to help reflect your creditworthiness.

What qualifies as a generally “good” credit score?

In general, a credit score of 670 to 739 is considered good according to FICO® standards. Scores in this range suggest that you are a responsible borrower with a solid history of managing credit well. 740 or higher is considered very good or exceptional. Remember, a higher the credit score usually results in more favorable mortgage rates and terms.

Additionally, a credit score between 580 and 669 is considered fair. This range aligns with many of the credit score requirements outlined above depending on the loan type. So don’t fall victim to the common mortgage myth that you need perfect credit to qualify for a home loan.

What’s the difference between a soft credit pull and hard credit pull?

When applying for a mortgage, lenders need to pull your credit report. There are two ways to do this:

- A soft credit pull is a credit check that doesn’t affect your credit score. It’s typically used for pre-qualifications or when you check your own credit. Supreme Lending has this option when you get pre-qualified for a mortgage.

- A hard credit pull, on the other hand, occurs when a lender reviews your credit score as a formal credit application during the loan approval process. Hard pulls can temporarily lower your credit score by just a few points. However, there’s no significant impact, which is another mortgage myth to debunk.

Here to Help

Don’t navigate the mortgage process alone! Our experienced and knowledgeable team at Supreme Lending is here to help you understand all aspects of your homebuying journey. From understanding credit score requirements and determining which loan program may work for you to our seamless underwriting process, we help you close your loan with confidence.

Contact us today to get started!

Related articles:

Common Credit Score and Down Payment Requirements by Mortgage Type

FHA Loans vs. Conventional Mortgage: Which One Is Right for You?

by SupremeLending | Jun 28, 2024

Understanding How to Use a Refinance Calculator

Refinancing a mortgage can be a strategic tool for many homeowners, but determining whether it’s the right move requires careful consideration and calculation. A refinance calculator can help you understand the potential costs and benefits of refinancing. Here’s an overview of what refinancing is, common reasons homeowners may consider refinancing, and how to use a refinance calculator to get an initial idea of potential related costs.

What Is Refinancing?

Refinancing a mortgage involves replacing an existing home loan with a new one, usually with different terms. The primary goals of refinancing are to change the loan term, reduce the interest rate, or tap into your home’s equity for cash. By refinancing, homeowners can potentially lower their monthly payments, pay off the mortgage sooner, or secure funds to use for other significant expenses. A refinance calculator can help breakdown the costs of refinancing and new estimated monthly payments.

Why Refi Today?

Even in today’s higher interest rate environment, there are still several reasons people may consider refinancing.

- Shorten Loan Term. Refinancing to a shorter loan term, for example going from a 30-year to a 15-year term, can help pay off the mortgage faster and save in interest over the life of the loan.

- Change Loan Type. Switching from an adjustable-rate mortgage (ARM) to a fixed-rate can provide more stability with consistent monthly payments. Borrowers may also refinance to change from a government-insured FHA loan to a Conventional mortgage or other eligible loan type.

- Cash-out Refinancing. This option allows borrowers to use the equity they’ve built in their home and receive the difference in cash to use for other expenses, such as home renovation projects, tuition, or additional large expenses.

- Lower Interest Rates. Securing a lower interest rate can reduce monthly payments and potentially save thousands of dollars in the long term.

- Life Changes. Major life events such as divorce or death may require refinancing to remove a co-signer from a loan. It’s important for married homebuyers to understand spousal states and ownership rights.

Using a Refinance Calculator**

A refinance calculator is a useful tool to help you understand and estimate potential costs associated with refinancing your current mortgage. Here are general steps to use a refinance calculator effectively.

1. Go to Supreme Lending’s online refinance calculator at www.SupremeLending.com > Learn > Calculators > Mortgage Refinance Calculator.

2. Input Current Loan Details, including the original loan balance, appraised value, interest rate, and loan terms.

3. Enter New Loan Information, including the proposed new mortgage terms, interest rate, and closing costs.

4. Calculate Monthly Payments. With the provided mortgage information, the calculator will provide an estimate of your new mortgage costs and monthly payment.

5. Compare Costs and Savings. The refinance calculator can help you review potential savings and total interest paid for the life of the loan. Consider the break-even point, which is the time it takes for your savings to cover the refinancing costs.

6. Evaluate Additional Factors. Consider any pre-payment penalties or other fees that may be applied to the current loan and the impact of extending or shortening the loan term. Additionally, if you used a down payment assistance program for your initial mortgage, be sure to refer back to the agreed upon terms. In some cases, the assistance may need to be paid back if refinancing before a specified period of time.

Calculate Refinancing Costs

When using a refinance calculator, it’s important to review associated costs to get an accurate picture of whether refinancing may be beneficial. Common refinancing costs include:

- Application Fee. This fee is charged to process the loan application.

- Origination Fee. The lender may charge a fee to process and originate the loan.

- Appraisal Fee. This is the cost of having a home appraised to determine its market value.

- Title Insurance and Search Fees. These are costs associated with verifying the home’s ownership and ensuring there are no outstanding claims on the property.

- Closing Costs. Other fees and charges may be included that can typically amount to 2-5% of the loan amount.

Determine Monthly Payments

The refinance calculator can also help you determine new estimated monthly payments. By comparing your current payment and the new projected calculation, you can see the impact on your loan and plan your budget accordingly. If the new payment is significantly lower, refinancing may be a great option. If the new payment is higher due to a shorter loan term or other factors, you may need to decide if the long-term benefits outweigh the upfront refinancing costs.

Refinancing a mortgage may offer benefits, but it’s essential to understand the costs and new loan terms involved. A refinance calculator may help you make an informed decision with a comparison of your current mortgage and proposed new loan. Take a step further and get pre-qualified with Supreme Lending today. Let us help you make the most of homeownership and explore your mortgage and refinancing options.

*By refinancing an existing loan, total finance charges may be higher over the life of the loan.

**Results received from this calculator are designed for comparative purposes only, and accuracy is not guaranteed. Supreme Lending is not responsible for any errors, omissions, or misrepresentations.

by SupremeLending | Apr 16, 2024

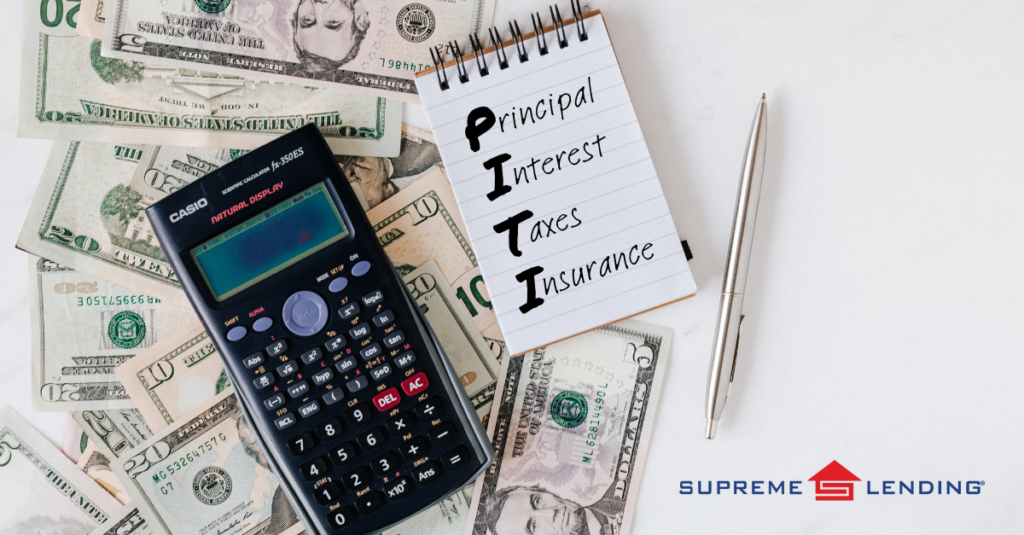

A mortgage is more than just the home loan amount, so let’s breakdown what all goes into a monthly payment beginning with the short acronym, mortgage PITI—principal, interest, taxes, and insurance. Understanding these factors can help you determine how much home you can afford and budget accordingly.

Principal (P):

Principal refers to the flat amount borrowed from a lender to purchase a home. It represents the initial loan amount, which is gradually paid down over the life of the mortgage through regular payments. Understanding the principal component of your mortgage payment is crucial for assessing the affordability of a home. A larger principal amount typically results in higher monthly mortgage payments, while a smaller principal amount may be more manageable depending on one’s budget.

Interest (I):

Interest is the rate percentage of how much you’ll pay each month as a fee for borrowing the funds. It is a fundamental component of mortgage payments. The interest rate on your mortgage directly impacts the total amount of interest paid over the life of the loan. A lower interest rate can reduce your monthly mortgage payments and lower the amount of interest you would pay over the life of the loan.

Taxes (T):

Taxes, specifically property taxes, are typically rolled into the monthly mortgage and vary by location and the appraised value of the home. These taxes fund various public services, such as schools, roads, and emergency services, within your community. Property tax rates fluctuate depending on the neighborhood and can have a significant impact on your overall housing expenses. Understanding property tax obligations associated with a prospective home is essential for accurate budgeting and planning.

Insurance (I):

Insurance, which can include both homeowners insurance and mortgage insurance, commonly have annual premiums that the lender can tie into your monthly payments. Homeowners insurance protects your investment by covering physical damages or loss to your property and belongings, such as fire, theft, or natural disasters. Mortgage insurance, which is typically required especially if you put less than 20% down, protects the lender if you default on the loan. Once you reach an agreed-upon equity threshold and loan-to-value ratio, it may be removed to lower your payments.

Practical Tips for Mortgage PITI

- Calculate Affordability. Using mortgage calculators and working with your Loan Officer can help provide an estimate for your monthly mortgage PITI payments based on your desired home price, down payment amount, interest rate, and other related terms.

- Factor in Additional Costs. In addition to PITI, consider other homeownership expenses, such as utilities, regular home maintenance, and homeowners association (HOA) fees, when establishing your housing budget.

- Build a Contingency Fund. Set aside savings for unexpected expenses or potential fluctuations in mortgage PITI payments, such as property tax increases or changes in insurance premiums.

- Reassess Periodically. Review your homeownership goals regularly and adjust as needed based on possible changes in income, expenses, interest rates, or market conditions.

Mortgage PITI—principal, interest, taxes, and insurance—serves as a fundamental framework for understanding the financial aspects of homeownership. Whether you’re a first-time homebuyer or a seasoned homeowner, examining each component of PITI offers valuable insights into how much home you can afford and helps you achieve your homeownership goals with confidence. Embrace the power of PITI as you embark on the exciting journey to owning your dream home.

Contact your local Supreme Lending branch to get started.