by First Integrity Team Supreme Lending | Jan 9, 2025

All You Need to Know About the FHA 203(h) Disaster Relief Loan Program

When natural disaster strikes, the devastation it leaves behind can be overwhelming, especially if your home is damaged or destroyed. At Supreme Lending, we know how difficult it can be to rebuild after such destruction. That’s where the FHA 203(h) Disaster Relief Loan may be able to help as an affordable option for those in eligible areas.

If you’ve been affected by disaster and are looking to rebuild or purchase a new home for a fresh start, Supreme Lending is here to help you navigate the challenging time with care and expertise. This guide will walk you through the FHA 203(h) loan, how it works, benefits, and why it may be a valuable program for helping disaster victims get back on their feet.

What Is the FHA 203(h) Disaster Relief Loan?

The FHA 203(h) is a government-insured mortgage program that provides financial assistance to individuals whose homes have been damaged or destroyed in federally declared disaster areas. This is designed to help homeowners and renters alike rebuild or purchase new homes in the wake of devastating events like hurricanes, floods, tornadoes, and wildfires.

What makes the FHA 203(h) Disaster Relief Loan unique is the ability to help make homeownership more attainable after such tragedy by offering flexible guidelines and 100% financing.

How Does FHA 203(h) Work?

The FHA 203(h) Disaster Relief Loan works similarly to other FHA programs but comes with added benefits and provisions specifically for disaster victims. Here’s a breakdown of how it works.

What Properties Are Eligible?

To qualify, your current home must be in a Presidentially Declared Major Disaster Area (PDMDA) and must have been damaged to the point where it is no longer livable. The loan must be secured within one year of the disaster declaration, offering you plenty of time to regroup and take the next step towards recovery.

Program Benefits

- No down payment required. One of the biggest benefits of this program is that there is no down payment requirement for eligible borrowers. This makes it easier to secure financing without the burden of saving for large upfront costs, especially after facing potential hardships caused by a disaster.

- Minimum credit score of 580. While there are still credit parameters in place, the FHA 203(h) offers more lenient requirements than other financing options. This may help borrowers whose credit was negatively impacted due to the natural disaster.

- Available for single-family or FHA-approved condos. The home must be a primary residence – either a single-family home or approved condominium project. This program is not designed for second homes or investment properties but is focused on truly helping homeowners get back on their feet.

- Purchase location flexibility. Through this program, it allows you to purchase a new home anywhere in the United States. The replacement home doesn’t have to be in a designated disaster area.

Combining FHA 203(h) with 203(k) Renovation

The FHA 203(h) program also offers the option to combine with an FHA 203(k) Standard or Limited Renovation loan. This involves adding renovation costs into a single mortgage to cover repairs and remodel projects ranging from minor updates to structural if approved. Plus, the damaged property is eligible regardless of the age of the home. It only needs to have been a habitable residence prior to the disaster.

Ready to Relocate or Rebuild?

Supreme Lending is here to help you move forward and rebuild when disaster strikes. To learn more about the FHA 203(h) Disaster Relief Loan or to go over other mortgage options, contact your local Supreme Lending branch today!

More Resources from the U.S. Department of Housing and Urban Development:

Related Articles:

by First Integrity Team Supreme Lending | Oct 17, 2024

Discover the Program Highlights of an FHA 203(k) Renovation Loan

Are you ready to turn a fixer-upper into your dream home? Whether it’s a home you’ve just bought or already own, renovation loans like the FHA 203(k) program may help you finance both the purchase and necessary repairs or updates all in one mortgage. Plus, the U.S. Department of Housing and Urban Development (HUD) announced that it is increasing the loan amount for Limited FHA 203(k) loans to $75,000 on all FHA case numbers effective November 4, 2024—that’s up from $35,000 which is huge news!

Here’s an in-depth look at how the FHA 203(k) renovation loan works, the differences between the Limited and Standard options, and what types of renovations may be covered.

What Is an FHA 203(k) Loan?

Insured by the Federal Housing Administration, the FHA 203(k) renovation loan allows homeowners to finance the cost of both the property and its renovations in a single loan. Whether you’re purchasing a home that needs updates or making repairs to your current home, this loan program may help make those dreams a reality. It offers the similar benefits of FHA loans for first-time buyers and repeat buyers alike. To qualify, eligible borrowers only need 3.5% down payment and there’s more lenient credit score requirements than other renovation loans.

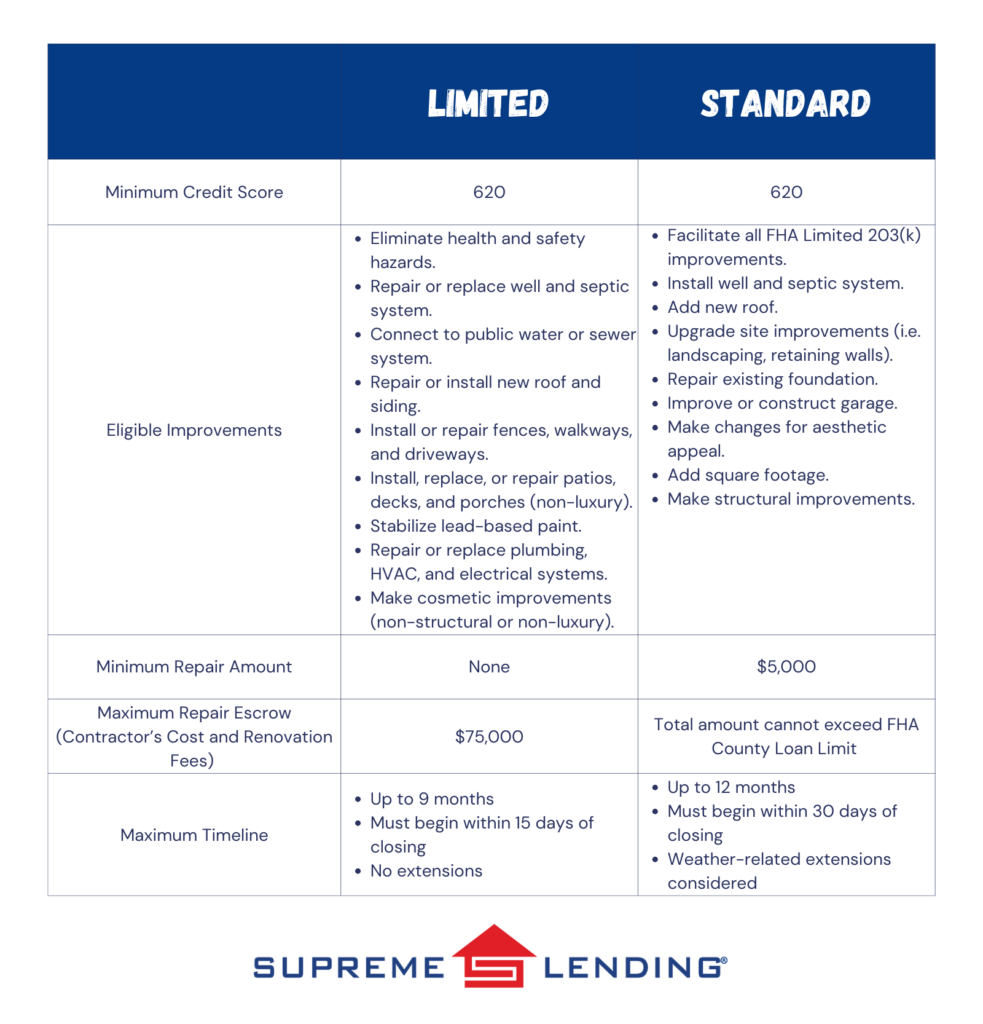

Limited vs. Standard FHA 203(k) Renovation Loan

There are two types of FHA 203(k) loans—Standard and Limited. Each has specific uses and limits depending on the scope of renovations you can make.

Limited FHA 203(k) Loan

The Limited 203(k) option is commonly used for smaller repairs and cosmetic upgrades. As mentioned, the loan amount will increase to $75,000 in November 2024, an exciting enhancement that will help open the door to renovations for more people. This loan covers non-structural projects such as remodeling kitchen fixtures, replacing flooring, painting, and minor landscaping. Unlike the Standard, the Limited program doesn’t require working with an HUD consultant or have a minimum loan amount.

Common Projects the Limited Covers

- Minor remodeling (i.e. updating kitchens or bathrooms)

- Replacing appliances or flooring

- Repainting or refinishing surfaces

- Energy-efficient improvements (i.e. installing new windows or insulation)

- Repairing roofs and gutters

Standard FHA 203(k) Loan

The Standard FHA 203(k) Renovation loan is more ideal for homes needing larger renovations and structural repairs. These may include adding rooms, replacing outdated plumbing or electrical systems, and fixing major structural issues. It has a minimum of $5,000 that must be used for renovations and the total loan amount must be within the FHA County Loan Limit. Because these projects are typically more complex, you’re required to work with an HUD-approved consultant.

Common Projects the Standard Covers

- Structural repairs or additions (i.e. adding on square footage or fixing foundation issues)

- Major systems replacements (i.e. plumbing, electrical, or HVAC systems)

- Roof repairs or replacements

- Modernization and improvements to the home’s function

- Accessibility improvements for people with disabilities

How Does the FHA 203(k) Renovation Loan Work?

The process for applying for an FHA 203(k) loan is similar to a regular FHA mortgage but comes with a few additional steps. Here’s an overview of how this loan program works.

- Find a property. Whether it’s a home you already own and want to refinance* or one you’re planning to purchase, identify a property that needs renovations.

- Get an appraisal. The home appraisal will assess both the home’s current market value as well as it’s “as-completed” value after the renovations are completed.

- Contractor and Estimates. Work with a licensed contractor to obtain the estimated costs for the repairs and improvements.

- Loan Application. You’ll apply for the loan based on the combined cost of the home and repairs.

- Renovation Timeline. Once the loan is approved, the renovation funds are placed into an escrow account and work begins. The renovation timeline can typically range from six months to one year.

*By refinancing an existing loan, total finance charges may be higher over the life of the loan.

FHA 203(k) Combined with FHA 203(h) Disaster Relief Loan

Did you know that eligible borrowers affected by federally declared disaster areas may be able to combine the FHA 203(k) renovation loan with the FHA 203(h) disaster relief loan? This means adding the renovation costs into a new mortgage if your home was destroyed and deemed unlivable. Plus, the damaged property is eligible regardless of the age of the home. It only needs to have been a habitable residence prior to the disaster.

Ready to Rebuild?

At Supreme Lending, we understand how important it is to transform a home into one that truly meets your needs. Whether you’re fixing up a new property or renovating your current home, the FHA 203(k) renovation loan offers an excellent way to finance those improvements. We’re proud to offer both Standard and Limited options to fit the scope of your home projects.

Want to learn more about FHA 203(k) renovation loans or other mortgage options? Contact our team at Supreme Lending today and get pre-qualified!

Looking for other renovation loan options? Read more:

by SupremeLending | Aug 1, 2024

When someone asks if it’s possible to add renovation costs to mortgage, the simple answer is yes! When buying a home, people dream of finding the perfect property that checks off all their boxes. However, sometimes the ideal property may need a little work to become that dream home. This is where renovation loans come in. By adding renovation costs to your mortgage, you can finance both the purchase of your home and the necessary improvements into a single loan. Read on to learn more about renovation loan options, benefits, and frequently asked questions.

Types of Renovation Loans

There are several loan programs to consider that can add renovation costs to your mortgage:

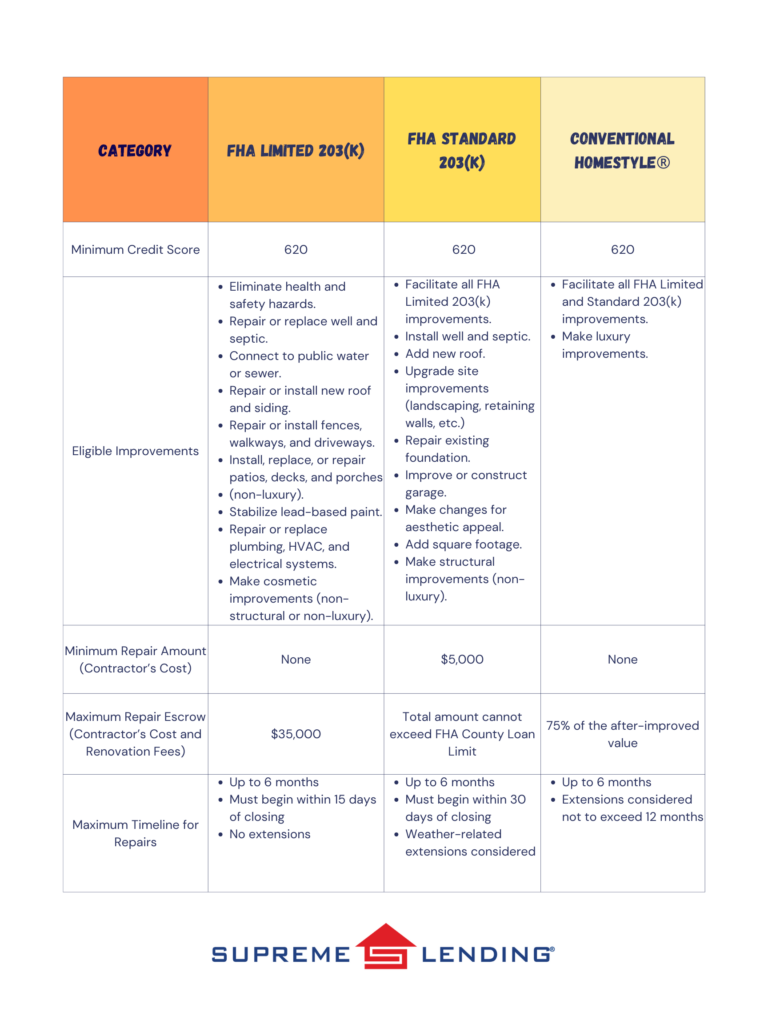

- FHA 203(k). This renovation program is an FHA loan, insured by the Federal Housing Administration. There are two options depending on the extent of the home remodel or repairs. The Limited 203(k) is for more minor updates that ensure the home is safe and functional and can include basic cosmetic improvements. The Standard 203(k) option offers more flexibility and larger scale renovations, such as structural foundation or adding square footage. Only primary residences are eligible. Click here to read more about the FHA 203(k) Renovation Loan.

- Fannie Mae HomeStyle®. This is a Conventional loan option to add renovation costs to mortgage. It includes home improvements that are permanently affixed to the property and add value, including luxury items such as high-end flooring, decks, fencing, a pool, etc. Unlike the FHA 203(k), this program can also be used toward qualified second homes and investment properties.

- VA Renovation. This renovation loan is for eligible military Veterans, active duty personnel, and some surviving spouses. It offers the same benefits as VA loans, such as no down payment requirements and lower closing costs, plus the ability to include certain home repairs into a single, affordable mortgage.

- Supreme Dream 203(k). Another exciting renovation loan program that Supreme Lending offers is the FHA 203(k) loan, as noted above, combined with the Supreme Dream down payment assistance resulting in less upfront costs.

How Renovation Loans Work

- Determine Your Renovation Needs. Assess the scope of your renovation project and obtain estimates from contractors to understand the anticipated costs.

- Loan Application. Apply for a renovation loan with a lender. You will need to provide detailed renovation plans. At Supreme Lending, we have a dedicated construction lending team to support all renovation loans for a smooth process.

- Loan Approval. Once approved, the loan amount is based on the projected value of your home after the renovations are completed.

- Renovation Process. Funds are typically disbursed in stages as the renovation progresses ensuring that contractors are paid, and the work is successfully completed.

- Final Inspection. After the renovations are finalized, a final inspection is typically required to verify that the work meets the loan requirements, and any remaining funds are released.

Frequently Asked Questions

Can I add renovation costs to any type of mortgage?

Not all mortgage types allow for renovation costs to be added. Specific loans, such as the programs listed above, are specifically designed to fund renovations and have additional steps and guidelines to follow.

How are renovation costs disbursed with a renovation loan?

With a renovation loan, funds for the purchase of the property are typically disbursed at closing. The renovation funds are placed in an escrow account to be paid out as repairs are completed.

How are renovation loans approved?

Your lender’s underwriting department will help approve the loan application and make sure all guidelines and requirements are met. This includes reviewing the home’s value after the renovations are made. The renovation schedule and documentation are also evaluated to ensure a seamless process.

Are there limits on the amount someone can borrow for renovations?

Yes. Each loan type has specific limits depending on the program. For example, an FHA 203(k) Limited loan currently has a maximum of $35,000* repair escrow amount to use toward the contractor’s costs and renovation fees. In turn, an FHA 203(k) Standard depends on the property’s FHA county loan limit. For Conventional renovation loans, the maximum renovation cost is typically up to 75% of the after-improved home value.

*Note: The FHA 203(k) Limited options will be increasing its maximum limit for renovation costs to $75,000 on or after November 4, 2024.

Click here for a complete guide to home renovation loans that includes a detailed comparison of FHA 203(k) and Conventional HomeStyle® loans.

Want to learn more about how to add renovation costs to your mortgage? Get started in creating your dream home with the help of Supreme Lending. We’re here to help every step of the way.

by SupremeLending | May 9, 2024

Learn why FHA loans may be a perfect option for first-time buyers.

While first-time buyers are hunting for their perfect home, they’ll also need to be on the hunt for the perfect mortgage—which may seem more overwhelming and not as enjoyable as touring properties. There are several financing options to choose from and programs available. It’s all about finding the one that fits best. At Supreme Lending, our goal is to provide the guidance you need to make informed decisions and be confident with your loan choice.

In this article, we’re highlighting a mortgage option that is designed specifically to help first-time buyers, FHA loans. Discover the many FHA loan benefits and why this option may be right for you.

Understanding FHA Loans: A Brief Overview

First, what exactly is an FHA loan? The Federal Housing Administration (FHA), a branch of the U.S. Department of Housing and Urban Development (HUD), insures FHA loans, which are issued by approved lenders. This insurance protects lenders against losses if a borrower defaults on their loan, making FHA loans less risky for lenders and consequently more accessible to first-time buyers.

FHA Loan Benefits

1. Low Down Payments.

To help overcome one of the biggest barriers for first-time homebuyers, FHA loans typically require a lower down payment compared to Conventional loans. This makes homeownership more accessible to people who may not have substantial savings or want to pay less upfront costs.

2. Flexible Credit Requirements.

FHA loans are more lenient when it comes to credit, allowing borrowers with lower credit scores to qualify for financing, which is beneficial for those who are still establishing their credit history. See common credit score and down payment requirements here.

3. Assumable Loans.

What does this mean? FHA loans are assumable, which means that if you sell your home, the buyer can take over your FHA loan, potentially offering them a competitive advantage in a rising interest rate environment. Restrictions on assumability may apply.

4. Lenient Debt-to-Income (DTI) Ratios.

DTI compares a borrower’s debt to their monthly income to measure’s their ability to manage monthly mortgage payments. FHA loans often allow for higher debt-to-income ratios compared to Conventional loans.

5. Lower Mortgage Insurance Premiums.

While FHA loans require mortgage insurance premiums (MIP), the premiums are often lower than those of Conventional loans, especially for borrowers with lower credit scores or smaller down payments. In fact, the FHA annual mortgage insurance premium was lowered from 0.85% to 055% in 2023 for most borrowers.

6. Seller Closing Cost Assistance.

Another benefit buyers could take advantage of is negotiating seller concessions to help cover upfront costs. FHA loans can allow sellers to contribute up to 6% toward the buyer’s down payment, appraisal fees, or other associated closing costs.

7. Gift Funds.

Gift funds are given to someone with no expectation of repayment, for example parents gifting their newlywed children money for a down payment. FHA loans allow borrowers to use gift funds from family members or other eligible sources to cover their down payment and closing costs. Note: A gift letter is required to confirm the gift funds.

8. Renovation Loans.

The FHA 203(k) Renovation loan is a home rehabilitation financing option, which allow borrowers to finance both the purchase price of the home and the cost of eligible renovations or repairs into a single loan. This helps buyers afford any necessary improvements and can open their home search to consider fixer-uppers.

9. Streamline Refinancing.

FHA loans offer a streamlined refinancing option, known as the FHA Streamline Refinance. This allows borrowers to refinance their current FHA loan with minimal paperwork and documentation, saving time and money.

10. No Prepayment Penalties.

FHA loans do not have prepayment penalties unlike some traditional mortgages. This allows borrowers to pay off their mortgage early without facing additional fees or charges, which can save money on interest over time.

11. 100% FHA Financing Available.

Did you know Supreme Lending offers two competitive FHA 100% financing options? Through the Chenoa Fund or the Supreme Dream program, these include a 30-year fixed-rate FHA loan paired with a second forgivable loan to be used toward down payment, closing costs, and prepaids.

These benefits make FHA loans an attractive option for first-time homebuyers, offering accessibility, flexibility, and affordability to achieve homeownership.

Ready to get started? Contact Supreme Lending today to learn more about FHA loans or other mortgage services we offer.

by SupremeLending | Mar 21, 2024

Picture this – you currently own or want to buy a home with good bones, but it needs some TLC. The good news is that you don’t have to handle a home remodel alone. Renovation loans are a great option to help fund home improvements, repairs, and enhancements by rolling the renovation costs into a single mortgage payment. It’s important to understand how renovation or home improvement loans work, types of renovation loan options, and benefits.

What Is a Renovation Loan?

Renovation loans are designed to help borrowers finance home improvement projects that will increase the value of the home. Whether you’re planning a small home makeover or extensive rehab project, a renovation loan combines a traditional purchase or refinance mortgage with the cost of renovations—it is an all-in-one mortgage financing option that covers the upfront costs of large repairs and projects.

Taking on the remodel before moving in can enhance your living space and home functionalities without the pressure of taking out an additional loan or paying out of pocket for costly repairs in the future.

Types of Renovation Loans

When it comes to renovation loans, there are a few options for prospective homebuyers and homeowners to consider based on eligibility, timing, and the scale of the home improvements needed.

FHA 203(k) Renovation

An FHA 203(k) loan, or an FHA rehab loan, is insured by the Federal Housing Administration and provides two options depending on the scope of the home improvement projects, including Limited 203(k) and Standard 203(k), offering different levels of renovation financing.

The minimum down payment for an FHA 203(k) loan is 3.5%. An FHA 203(k) loan covers common basic home improvements and repairs but excludes larger luxury projects and amenities. The Limited option has no minimum renovation amount and can cover up to $35,000 in renovation costs. The Standard has expanded eligible improvements including some structural upgrades and a minimum renovation cost of $5,000. Typically, all renovations must be completed within 6 months.

VA Renovation

The Department of Veterans Affairs (VA) also has a Renovation loan option. A VA Renovation loan offers 100% financing for eligible U.S. Veterans or military personnel to cover a mortgage combined with planned renovation costs into a single loan. Eligible home improvements are similar to FHA 203(k) to cover common upgrades that will make the property safer, healthier, or more functional, excluding luxury projects. VA Renovation loans can finance up to $50,000 in home repair costs.

Conventional Renovation

A Conventional Renovation loan, such as Fannie Mae’s HomeStyle® program, is another financing option that rolls the costs of home renovation projects into a single mortgage and offers more flexibility than a government loan. Conventional Renovation mortgages can cover larger, luxury upgrades, such as creating a high-end bathroom or kitchen with decorative tilework or adding a sparkling backyard pool. The maximum home repair amount is 75% of the home’s post-construction appraised value.

More Benefits of Renovation Loans and Remodeling

- Expand Your Home Search. Prospective homebuyers may have a broader range of properties to choose from, including fixer-uppers, knowing that they could finance custom home upgrades or needed repairs with a Renovation loan.

- Save on Upfront Costs. Home renovation projects can be costly. Funding home remodeling projects with your mortgage could help keep you from tapping into your personal savings and avoid hefty upfront repair costs.

- Grow Your Home Value. Renovation loans are intended to increase the value of your home, which may result in a smart, long-term investment and the potential to build more equity.

- Personalize Your Dream Home. Renovation loans offer an affordable option to help make your design visions come to life and beautify your home to fit your character.

- Enhance Comfort and Livability. Whether it’s expanding a kitchen, adding a bathroom, or creating a home office space, upgrading your home can add modern conveniences and improve your overall well-being.

If you’re looking to enhance your living spaces and potentially increase your property value, a Renovation loan could be the answer to creating the home of your dreams. To learn more about renovation financing or other mortgages, contact your local Supreme Lending branch today.

Related Articles: