by SupremeLending | Jun 13, 2024

Condo financing is an exciting and rewarding experience, especially if you’re looking to purchase a dream home with low maintenance and community amenities. It’s important to understand how condo loans work to make an informed decision in your homebuying journey. Let Supreme Lending help guide you through the condo financing process. Explore the steps involved, go over frequently asked questions about condo loans, and discover perks of condo living.

What Is a Condo Loan?

Condo financing is similar to traditional mortgages but comes with a few unique factors. A condo loan is specifically designed for purchasing a condominium unit. Lenders handle condo loans slightly differently due to the shared ownership structure and the condo association, also known as the homeowners’ association (HOA).

When applying for a condo mortgage, lenders will not only consider your credit report and financial profile but also the condition and management of the condo complex. This includes the association’s budget, reserves, and overall governance. A condo loan covers the unit itself and may include additional fees associated such as HOA dues.

Condo Financing Process

Here’s a quick, step-by-step guide of how condo financing works.

1. Get Pre-Qualified.

As with any mortgage, typically the first step is pre-qualification or pre-approval. This helps you understand how much home you may be able to afford and shows sellers you’re a serious, capable buyer.

2. Find the Right Condo.

Once you know your budget, search for condos that fit your preferences, location, and lifestyle. Ensure the condo is on a lender-approved list or can meet lender requirements.

3. Apply for a Loan.

Submit your full mortgage application with all required documentation, such as income verification, credit history, and details about the condo.

4. HOA Condo Review.

The lender will review the condo HOA’s financial statements, bylaws, insurance policies, and reserve funds to ensure the property is a sound investment and isn’t deemed high risk.

5. Appraisal and Inspection.

An appraisal will determine the condo’s market value, and a home inspection will help identify any potential issues with the property, such as safety hazards or systems that may not be working properly.

6. Close on the Loan.

Once all criteria are met, you’ll proceed to closing where you’ll sign the necessary documents and transfer ownership of the condo. Congratulations, you’re a condo owner!

Condo Financing FAQs

How does condo financing differ from traditional mortgages?

While similar to a conventional mortgage, a condo loan requires additional review of the condo association’s finances, bylaws, and occupancy rates. This will ensure lenders that the complex is stable and well-managed, which helps mitigate lending risks.

What’s the difference between warrantable and non-warrantable condo loans?

A warrantable condo means that the complex meets the criteria set by Fannie Mae and Freddie Mac, the government-sponsored enterprises (GSEs) that purchase and guarantee mortgages from lenders. A warrantable condo typically has at least 50% of units that are owner-occupied or second homes, and the homeowners’ association management is financially secure. Non-warrantable condos do not meet these guidelines.

Can I still finance a non-warrantable condo?

Yes. Borrowers may face unique challenges when it comes to financing non-warrantable condos, condotels, and co-ops. However, Supreme Lending offers a wide range of condo loan programs, including non-warrantable condos and FHA spot approval processing.

Can I use an FHA or VA loan to buy a condo?

Yes. There are options to finance condos through FHA or VA loans. However, the condo complex must be on an approved list by the FHA or VA. If it’s not approved by the FHA, Supreme Lending may be able to provide FHA Single-Unit Approvals to help get a condo unit approved quicker.

Are interest rates higher for condo loans?

Interest rates for condo loans may be slightly higher than single-family mortgages due to the perceived higher risk. However, rates vary based on market conditions, credit score, and individual lenders, so be sure to work with an experienced, professional Loan Officer to go over your options.

Does Supreme Lending have an in-house condo loan team?

Yes! Supreme Lending has a dedicated, in-house Condo Project Review team to manage the condo financing process. This includes reviewing the complex and HOA to make sure the property’s guidelines are met.

Benefits of Condo Living

- Community Living. Condos often foster a strong sense of community, providing ample opportunities to meet neighbors and participate in social activities.

- Lower Maintenance. The Condo’s HOA typically handles exterior maintenance such as landscaping and select repairs, freeing you from traditional homeownership responsibilities.

- Condos can offer several amenities such as swimming pools, gyms, and recreational areas, allowing you to enjoy these perks without the personal investment or upkeep.

- Prime Locations. Condos are often located in desirable, urban areas, offering convenient proximity to work, entertainment, and dining options.

Condo financing can unlock the door to a vibrant and accessible lifestyle. By understanding the ins and outs of the condo loan process, you can be equipped with knowledge and power to make informed decisions. At Supreme Lending, we’re here to help guide you through every step of condo financing.

by SupremeLending | Jun 10, 2024

When it comes to financing your new home, choosing the right mortgage is so important – FHA loans, Conventional mortgages, down payment assistance – there are several options to choose from. Each loan program has its own set of guidelines, benefits, and considerations. Comparing loan types can help you make an informed decision of what may fit your needs and homeownership goals. Let’s examine the difference between these two popular options: FHA loans and Conventional mortgages.

What Is an FHA Loan?

FHA loans are mortgages insured by the U.S. government’s Federal Housing Administration (FHA) against borrower default. They are designed to help more people who may not qualify for Conventional loans achieve homeownership. Here are some key benefits of FHA loans:

- Lower Credit Score Requirements. FHA loans typically require a minimum credit score of 580, which is lower than Conventional loans.

- Low Down Payment. One of the most attractive highlights of FHA loans is the low down payment requirement. Qualified borrowers can put down as little as 3.5% of the purchase price, plus there may be options to include down payment assistance.

- Flexible Debt-to-Income (DTI) Ratio. FHA loans allow higher DTI ratios, making it more feasible for borrowers with existing debt to qualify.

- Assumable Loans. FHA loans are assumable, meaning if you sell your home, the buyer can take over your existing FHA loan. This could potentially help save buyers money on closing costs and interest.

- More Lenient Qualification Requirements. In general, the qualification criteria for FHA loans is more moderate compared to Conventional loans. This helps a broader range of borrowers become homeowners.

What Are Conventional Loans?

Conventional mortgages are loans not insured or guaranteed by any government agency unlike FHA. They are offered by private lenders. Borrowers typically need to have a higher credit score and lower DTI ratio.

- Lower Mortgage Insurance Costs. While FHA requires mortgage insurance premiums (MIP) for the life of the loan, Conventional loans typically only require private mortgage insurance (PMI) until the borrower buys down 20% of the mortgage.

- Higher Loan Limits. Conventional loan borrowers can generally qualify for higher loan limits compared to FHA. This can help borrowers purchase more expensive homes.

- Variety of Loan Terms. Conventional mortgages offer a wide range of loan terms and options, including fixed-rate and adjustable-rate mortgages (ARMs), providing more flexibility.

- Potential for Lower Interest Rates. Borrowers with higher credit scores and larger down payments can often secure lower interest rates with Conventional loans than FHA.

- Conforming & Non-Conforming Options. Conforming conventional loans meet the guidelines of government-sponsored enterprises (GSE), such as Fannie Mae and Freddie Mac. While non-conforming loans do not and can have higher loan amounts, including Jumbo loans.

Frequently Asked Questions About FHA vs. Conventional Loans

Which loan is better suited for first-time homebuyers?

FHA loans are often a great option for first-time buyers due to their lower credit score and down payment options. They provide a pathway to homeownership for those who may not initially qualify for a Conventional loan.

Can I refinance* my FHA loan into a Conventional mortgage?

Yes! Borrowers can refinance an FHA loan into a Conventional one. This could potentially eliminate the FHA’s mortgage insurance requirement if you have enough equity in the home and lead to more flexible terms.

*By refinancing an existing loan, total finance charges may be higher over the life of the loan.

Are there income limits for FHA or Conventional?

FHA mortgages don’t have income limits, but they may have loan limits based on the location of the property. Conventional loans don’t have income limits either, however higher income and a better credit profile can help you qualify for a larger loan amount.

How do I decide which loan is right for me?

Take into concentration your credit score, funds you have for down payment and closing costs, and long-term goals. FHA can be ideal for those with lower credit scores, while Conventional loans may be better suited for borrowers with stronger credit profiles. Getting pre-qualified with Supreme Lending can help give you estimated costs for each option.

Whether you opt for an FHA loan or a Conventional, both options provide pathways to owning your dream home. It’s important to review your current situation, consider the benefits of different loan types, and work with a knowledgeable loan officer to help guide you through the mortgage process.

At Supreme Lending, we’re committed to helping you navigate the homebuying process with ease. Contact your local branch to get started today!

by SupremeLending | Jun 5, 2024

Understanding a Bank Statement Loan

For entrepreneurs and self-employed individuals, securing a mortgage can often be a challenge. Traditional home loans typically require W-2 tax returns and other documentation that may not accurately reflect the income of self-employed borrowers. This is where Supreme Lending’s bank statement loans come in. Designed for those who run their own businesses, bank statement loans offer an alternative option for self-employed homebuyers without the need for conventional income and tax documentation. Here’s everything you need to know about bank statement mortgages.

What Is a Bank Statement Loan?

A bank statement loan, commonly known as a self-employed mortgage, is a type of home loan designed for those who may have non-traditional sources of income. Simply put, instead of relying on W-2 forms and tax returns, lenders use the borrower’s bank statements to verify their income to approve the loan. This allows self-employed individuals to qualify for a mortgage based on their cash flow rather than their taxable income, which may be reduced by business expenses and tax deductions.

How Do Bank Statement Mortgages Work?

Income Verification

For these types of loans, lenders typically review the past 12 to 24 months of your personal or business bank statements to determine your average monthly income. This provides an accurate picture of your financial health and ability to repay the loan and make monthly mortgage payments.

Down Payment Requirements

The down payment requirements for bank statement loans can vary depending on the lender, but it can generally range from 10% to 20%. A larger down payment amount can sometimes secure more favorable terms and interest rates.

Credit Score and Other Requirements

While these loans are designed to be a more flexible homebuying option, mortgage professionals will still review your credit score, assets, and other financial factors to assess the potential lending risk. A higher credit score may increase your chances of approval for the loan.

Common FAQs and Considerations

Who Can Benefit from a Bank Statement Mortgage?

As mentioned above, these loans are ideal for self-employed borrowers, including small business owners, corporation owners, freelancers, and gig economy workers whose income may be substantial, but not consistently documented like W-2 employees. It’s a great option if you have strong cash flow but your tax returns don’t reflect your true income due to tax write-offs and deductions.

What Types of Properties Can Qualify?

These loans can be used to purchase various types of properties, including single-family homes, condos, townhouses, and in some cases multi-family properties. There are also options for second homes and investment properties depending on the loan type. Each lender has specific property requirements and guidelines, so it’s important to work with a knowledgeable loan officer to help guide you through the process.

What Are Interest Rates?

Interest rates for bank statement loans may be higher than those for Conventional loans due to the potential increased risk to lenders. However, if a borrower has a strong financial profile, it may be possible to lock in a more competitive rate. Additionally, rates are typically lower for a 24-month bank statement loan versus 12 months.

How Is Income Calculated?

For bank statement mortgages, lenders will typically sum up your total deposits over the selected period of time (12 to 24 months) and divide by the number of months to calculate your average monthly income. Business-related expenses and unusual deposits may be excluded to ensure a more accurate income assessment.

What If My Spouse Is a W-2 Employee?

Depending on the loan program and circumstances, lenders may consider a spouse’s income as well when calculating their joint eligibility for a bank statement loan. For example, a business owner’s average monthly income and a spouse’s W2s, paystubs, and employment verification could both be used to determine their combined income.

Benefits of Bank Statement Lending

Owning your own business is part of the American Dream. However, business owners may not qualify for a traditional mortgage to buy their American Dream Home. Bank statement loans offer that freedom. They give self-employed borrowers flexibility to use their true income without being tied down by tax deductions or business expenses. It also opens the door to homeownership for more people in the community—whether it’s their first home or tenth.

If you’re self-employed and ready to explore your mortgage options, contact Supreme Lending today. We’re here to help you navigate the process and find the best loan option to fit your unique needs.

Related Articles:

by SupremeLending | May 31, 2024

The Ultimate Mortgage DTI Handbook

When it comes to securing a mortgage, understanding your finances has never been more important. One of the most important metrics lenders use when evaluating a borrower’s eligibility for a mortgage is Debt-to-Income ratio, commonly known as DTI. Let’s dive into what exactly mortgage DTI is, how it’s used, what sources of debt and income are considered, and what establishes a fair or good DTI. Plus, we’ll offer some helpful tips for potential homebuyers on understanding their DTI.

What Is Debt-to-Income (DTI) Ratio?

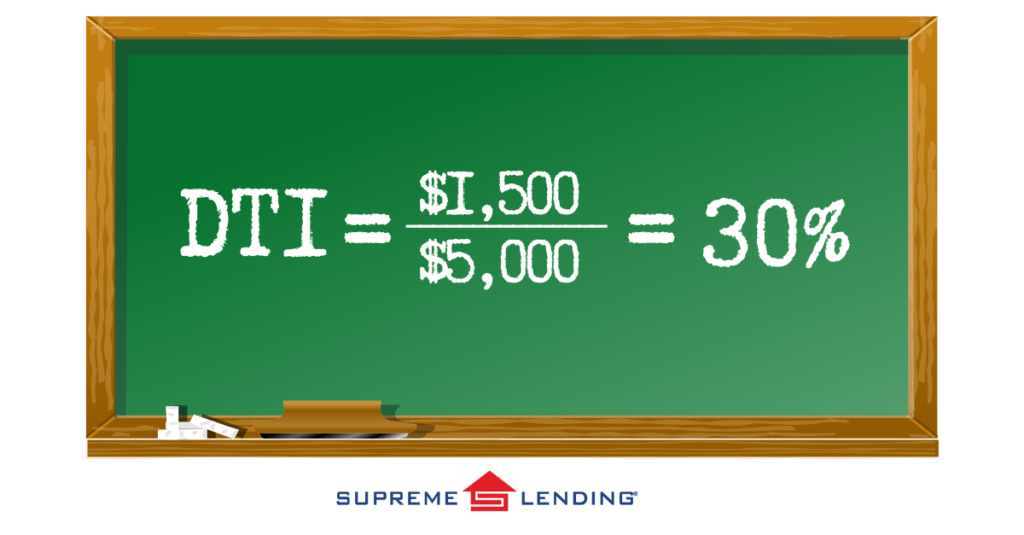

DTI is a financing metric that compares an individual’s monthly debt payments to their gross monthly income. Essentially, it measures the percentage of your income that goes toward paying off debts. Lenders use DTI to assess a borrower’s ability to make monthly payments to repay the loan. DTI is calculated by dividing your total monthly debt payments by your gross monthly income and multiplying the result by 100 to get the ratio percentage.

For example, if you have $1,500 in monthly debt payments and a gross monthly income of $5,000, your DTI would be 30%, as calculated below:

How DTI Is Used to Determine Mortgage Eligibility

Lenders look at your DTI to evaluate your ability to take on additional debt in the form of a mortgage. A lower DTI indicates that you have a good balance between debt and income, resulting in a more attractive and capable buyer. There are DTI thresholds that borrowers will need to meet, which can vary by lender or specified by the loan program guidelines.

Types of Mortgage DTI

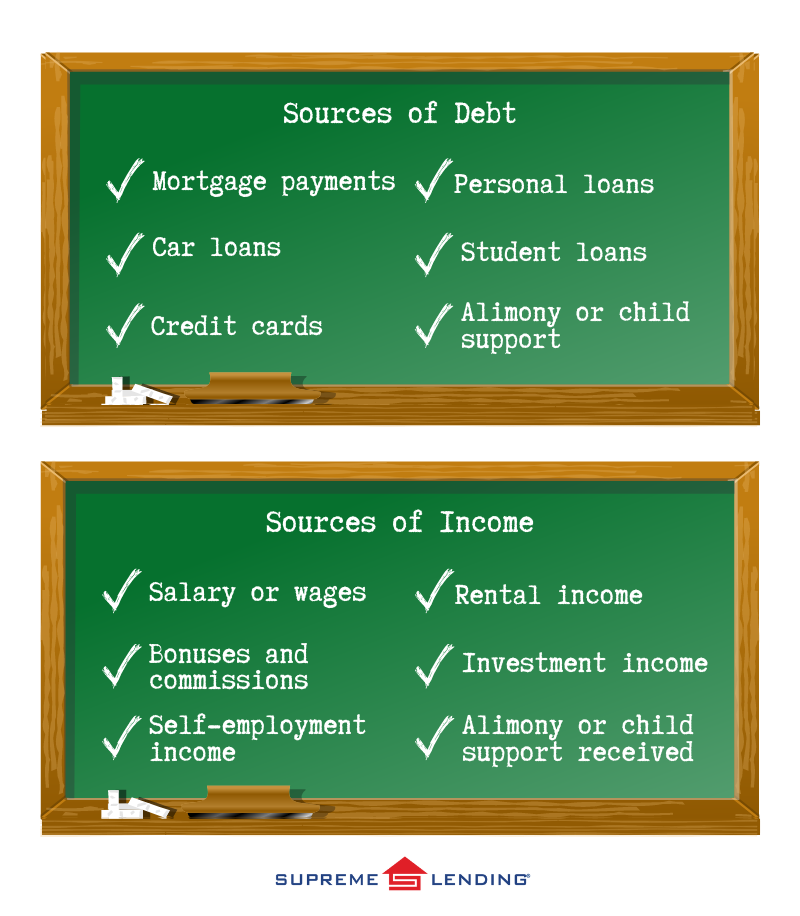

- Front-end DTI: Also called a housing ratio or mortgage-to-income, this ratio only calculates housing-related expenses, such as the monthly mortgage payment, property taxes, homeowners’ insurance premiums, and homeowners association fees, if applicable, relative to your gross monthly income.

- Back-end DTI: This ratio includes all your monthly debt obligations, such as credit card payments, car loan payments, and student loan debt, in addition to the housing-related debt. Lenders typically focus more on back-end DTI when evaluating a buyer’s capability to repay a loan as it provides a clearer picture of their financial responsibilities.

Sources of Debt and Income Considered

What Is Considered a Favorable DTI?

A good DTI ratio for a mortgage depends on the type of loan and the lender. Most lenders prefer a back-end DTI of around 36% or less, though some may accept higher ratios, especially for borrowers with strong credit scores or significant assets.

Helpful Mortgage DTI Tips for Potential Homebuyers

1. Avoid New Debt

Before applying for a mortgage, calculate your current DTI to give you a rough understanding of where you stand. This will help identify if you need to make any adjustments to potentially improve your DTI ratio before deciding to purchase a home.

2. Reduce Outstanding Debts

Paying down existing debts can significantly improve your DTI. Consider focusing on reducing or eliminating higher interest debts like credit card balances first.

3. Increase Your Income

Look for opportunities to boost your income. This could be through a salary increase, getting a higher-paying job, adding a part-time gig, or exploring other income sources.

4. Avoid New Debt

Refrain from taking on new debt before applying for a mortgage and during the loan approval process. New loans or credit lines may have an impact on your DTI and mortgage eligibility.

5. Seek Professional Advice

Consult with a financial professional for personalized guidance or a loan officer to get a better understanding of your DTI and loan program requirements. There may be other mortgage options better suited for you depending on your goals, such as Debt Service Coverage Ratio (DSCR) loans for investment properties that don’t use DTI.

6. Consider a Co-Signer

If your DTI is in the higher range, you may benefit from having a co-signer who has a higher income or less debt to contribute.

7. Understand Loan Programs

Guidelines and criteria to qualify for a mortgage vary depending on the program and lender. For example, FHA loans typically have more lenient DTI requirements than Conventional loans. Work with our team at Supreme Lending to explore a variety of different mortgage options and find the one best fit for you.

Managing Your Debt-to-Income Ratio

Understanding mortgage DTI and your Debt-to-Income ratio is essential for navigating the loan process. By managing your DTI and making informed decisions, you may potentially improve your mortgage eligibility and chances of securing your dream home.

Contact Supreme Lending to learn more about how we can help you achieve your homeownership goals with confidence.

Related articles:

by SupremeLending | May 13, 2024

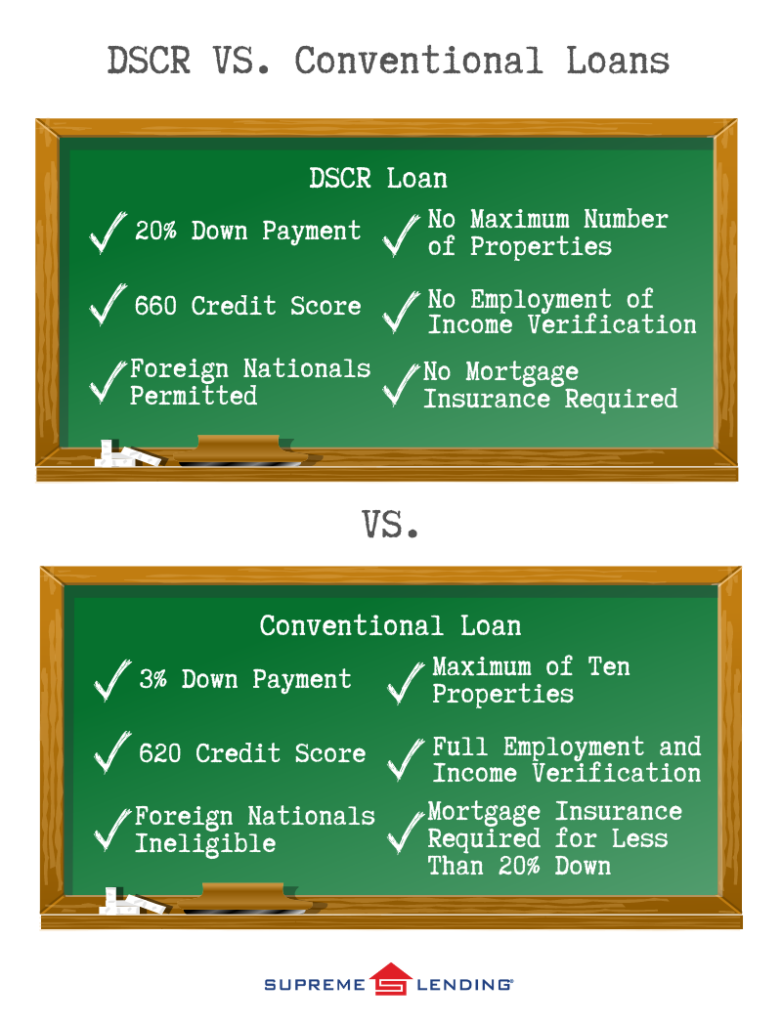

An Investor’s Guide for DSCR loans

Whether you’re just getting started with your investment portfolio or are a seasoned investor, navigating real estate is all about strategy. Supreme Lending is proud to offer a program to help investors easily finance dream investment homes without a traditional mortgage: the Debt Service Coverage Ratio (DSCR) loan. Here’s a guide for everything you need to know about DSCR loans, how they work, and the benefits they offer for investors looking to maximize returns.

DSCR Loan Basics

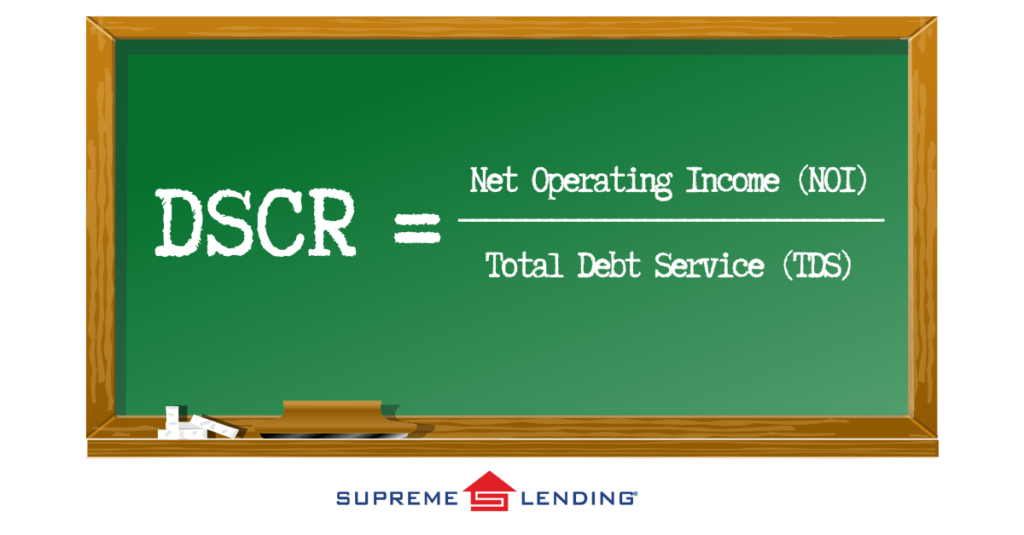

Simply put, DSCR is the ratio of a property’s rental income to its mortgage payment, taxes, and insurance. This helps lenders measure an investor’s ability to cover the mortgage from the cash flow generated from the property.

DSCR is similar to Debt-to-Income (DTI) for typical mortgages. However, the difference is that for a traditional loan, the percentage to service the debt is dependent on the borrower’s personal income, whereas for income-producing properties, it’s based on the property’s income. No income or employee verification is needed.

How To Calculate DSCR

To calculate the DSCR, divide the property’s net operating income (NOI) by its total debt service (TDS). The formula is as follows:

A DSCR of 1.0 indicates that the property’s net operating income is exactly equal to its debt obligations. A DSCR greater than 1.0 signifies that the property generates more income than needed to cover its debt payments, while a DSCR below 1.0 indicates insufficient income to cover debt payments. Typically, rates of 1.25 or greater are ideal and borrowers may receive better pricing with a higher ratio.

Eligibility for DSCR Loans

While guidelines to qualify for DSCR loans vary by lender, here’s an overview of common program highlights of Supreme Lending’s DSCR offering.

- Eligible borrowers include both first-time and experienced investors, but first-time homebuyers do not qualify.

- Foreign Nationals can qualify if eligible.

- First-time investors allowed at 75% Loan-to-Value (LTV).

- 20% down payment required; 25% for first-time investors.

- Vesting in entities permitted such as partnerships or LLCs (Limited Liability Company).

- Purchase and refinance options available.

- Investment, income-producing properties only.

Why Choose a DSCR Loan?

Prospective borrowers for DSCR loans may be looking to take advantage of home investments and generate rental income. For example:

- Borrowers looking to start their real estate investment portfolio.

- Investors looking to expand their current real estate portfolio.

- Eligible Foreign Nationals looking for an investment opportunity in the U.S.

- Borrowers in an LLC looking to invest in a property with their business partner.

- Investors pursuing niche strategies like short-term rentals or the BRRRR (Buy, Rehab, Rent, Refinance, Repeat) Method.

Benefits of DSCR Loans for Investors

- No documentation of income or employee verification versus conventional investment property loans, saving time and less documentation.

- No maximum number of properties—the sky is the limit!

- No mortgage insurance required compared to other loan options.

By evaluating a property’s ability to generate income relative to its debt obligations, DSCR loans provide valuable insights and savvy financing for investors—both first-time and seasoned investment professionals.

Contact your local Supreme Lending branch to learn more about DSCR loans and other mortgage options

by SupremeLending | May 9, 2024

Learn why FHA loans may be a perfect option for first-time buyers.

While first-time buyers are hunting for their perfect home, they’ll also need to be on the hunt for the perfect mortgage—which may seem more overwhelming and not as enjoyable as touring properties. There are several financing options to choose from and programs available. It’s all about finding the one that fits best. At Supreme Lending, our goal is to provide the guidance you need to make informed decisions and be confident with your loan choice.

In this article, we’re highlighting a mortgage option that is designed specifically to help first-time buyers, FHA loans. Discover the many FHA loan benefits and why this option may be right for you.

Understanding FHA Loans: A Brief Overview

First, what exactly is an FHA loan? The Federal Housing Administration (FHA), a branch of the U.S. Department of Housing and Urban Development (HUD), insures FHA loans, which are issued by approved lenders. This insurance protects lenders against losses if a borrower defaults on their loan, making FHA loans less risky for lenders and consequently more accessible to first-time buyers.

FHA Loan Benefits

1. Low Down Payments.

To help overcome one of the biggest barriers for first-time homebuyers, FHA loans typically require a lower down payment compared to Conventional loans. This makes homeownership more accessible to people who may not have substantial savings or want to pay less upfront costs.

2. Flexible Credit Requirements.

FHA loans are more lenient when it comes to credit, allowing borrowers with lower credit scores to qualify for financing, which is beneficial for those who are still establishing their credit history. See common credit score and down payment requirements here.

3. Assumable Loans.

What does this mean? FHA loans are assumable, which means that if you sell your home, the buyer can take over your FHA loan, potentially offering them a competitive advantage in a rising interest rate environment. Restrictions on assumability may apply.

4. Lenient Debt-to-Income (DTI) Ratios.

DTI compares a borrower’s debt to their monthly income to measure’s their ability to manage monthly mortgage payments. FHA loans often allow for higher debt-to-income ratios compared to Conventional loans.

5. Lower Mortgage Insurance Premiums.

While FHA loans require mortgage insurance premiums (MIP), the premiums are often lower than those of Conventional loans, especially for borrowers with lower credit scores or smaller down payments. In fact, the FHA annual mortgage insurance premium was lowered from 0.85% to 055% in 2023 for most borrowers.

6. Seller Closing Cost Assistance.

Another benefit buyers could take advantage of is negotiating seller concessions to help cover upfront costs. FHA loans can allow sellers to contribute up to 6% toward the buyer’s down payment, appraisal fees, or other associated closing costs.

7. Gift Funds.

Gift funds are given to someone with no expectation of repayment, for example parents gifting their newlywed children money for a down payment. FHA loans allow borrowers to use gift funds from family members or other eligible sources to cover their down payment and closing costs. Note: A gift letter is required to confirm the gift funds.

8. Renovation Loans.

The FHA 203(k) Renovation loan is a home rehabilitation financing option, which allow borrowers to finance both the purchase price of the home and the cost of eligible renovations or repairs into a single loan. This helps buyers afford any necessary improvements and can open their home search to consider fixer-uppers.

9. Streamline Refinancing.

FHA loans offer a streamlined refinancing option, known as the FHA Streamline Refinance. This allows borrowers to refinance their current FHA loan with minimal paperwork and documentation, saving time and money.

10. No Prepayment Penalties.

FHA loans do not have prepayment penalties unlike some traditional mortgages. This allows borrowers to pay off their mortgage early without facing additional fees or charges, which can save money on interest over time.

11. 100% FHA Financing Available.

Did you know Supreme Lending offers two competitive FHA 100% financing options? Through the Chenoa Fund or the Supreme Dream program, these include a 30-year fixed-rate FHA loan paired with a second forgivable loan to be used toward down payment, closing costs, and prepaids.

These benefits make FHA loans an attractive option for first-time homebuyers, offering accessibility, flexibility, and affordability to achieve homeownership.

Ready to get started? Contact Supreme Lending today to learn more about FHA loans or other mortgage services we offer.