by SupremeLending | Jul 29, 2024

If you’re thinking of buying a home, you may want to consider the possibility of seller concessions to help reduce upfront loan expenses. Imagine having a portion of your mortgage closing costs covered or even getting some essential home repairs taken care of without having to dig into your savings. That’s where seller concessions come in, also known as seller assistance. It can be a significant benefit for both buyers and sellers. In this guide, we’ll explore what seller concessions are, seller assist limits, and frequently asked questions.

What Are Seller Concessions?

Seller concessions are contributions paid by the seller that go toward the homebuyer’s closing costs. These can include closing fees, prepaid expenses, or even home repairs or improvements. These concessions can help lower the amount of money a buyer needs to bring to the closing table, making the home purchase more affordable.

The concession amount can be expressed as a percentage of the home’s purchase price or fixed dollar amount.

Examples of What Seller Concessions Can Cover

Seller concessions can be used for a variety of mortgage and homebuying costs including:

- Loan Origination Fees. Fees charged by the lender for processing the loan application.

- Appraisal Fees. This is the cost of having a home appraised.

- Home Inspection Fees. This is the cost of having a home inspected before closing.

- Property Taxes. Prepaid property taxes may be included in closing.

- Title Insurance. This insurance protects the buyer and lender from potential disputes over ownership.

- Discount Points. Also known as mortgage points, these help pay down the interest rate using upfront costs.

- Home Repairs or Improvements. Costs for necessary repairs identified during the home inspection or agreed-upon improvements before the sale.

How Do They Work?

- Negotiation. Seller concessions are typically negotiated as part of the buyer’s and seller’s purchase agreement. This request can be made with help from a real estate agent.

- Agreement. If the seller agrees to concessions, the specific details are outlined in the contract and must not exceed a specified limit depending on the loan type.

- Appraisal. The agreed-upon concessions cannot inflate the property’s value. Lenders require an appraisal to ensure the property’s market value supports the loan amount, including the concessions.

- Loan Approval. The lender will review the agreement and appraisal. This will ensure that the concessions align with the mortgage program’s guidelines.

- Closing. When the loan is ready to close, the costs are applied to the buyer’s closing costs or other agreed-upon expenses.

Who Benefits from Seller Concessions?

Both the buyers and sellers can benefit!

- Buyers. Concessions can lower the upfront costs needed to buy the home, making it easier to afford the property.

- Sellers. Offering concessions can also make the home more attractive for potential buyers, helping sell the home quicker.

Seller Assistance Limits

Limits on how much a seller can contribute vary depending on the loan type and down payment:

Conventional Loans

- Primary residence and second homes:

- 3% maximum with less than 10% down

- 6% maximum with 10-25% down

- 9% maximum with more than 25% down

- Investment properties:

- 2% maximum regardless of down payment

FHA/USDA Loans

- 6% maximum toward closing costs and prepaid items

VA Loans

- 4% maximum toward prepaid items

- No limit for closing costs or reasonable discount points

Frequently Asked Questions

Can the seller cover the entire down payment?

No. Seller concessions cannot be used for the full down payment. They are typically used for closing costs, prepaid expenses, and other associated fees, while meeting the loan guideline limits.

Does seller assistance affect the loan approval process?

Seller concessions themselves do not affect loan approval, but lenders can consider the impact on the Loan-to-Value (LTV) ratio and may require specific guidelines.

How does it impact the home appraisal?

The home’s appraisal must support the purchase price, including any seller contributions. If the appraised value is lower than the agreed-upon price, the lender may require adjustments.

Can a buyer negotiate for concessions?

Yes! Homebuyers can request this during negotiations. It’s essential to work with a knowledgeable real estate agent to help navigate the process.

How do seller concessions benefit first-time homebuyers?

First-time buyers often benefit from this as they may have limited funds for closing costs and other expenses. Seller assistance is another great way for more people to unlock the door to homeownership!

If you’re ready to start your homebuying journey, your local Supreme Lending team is ready to help! Contact us to learn about your mortgage options and get pre-qualified today.

by SupremeLending | Jul 26, 2024

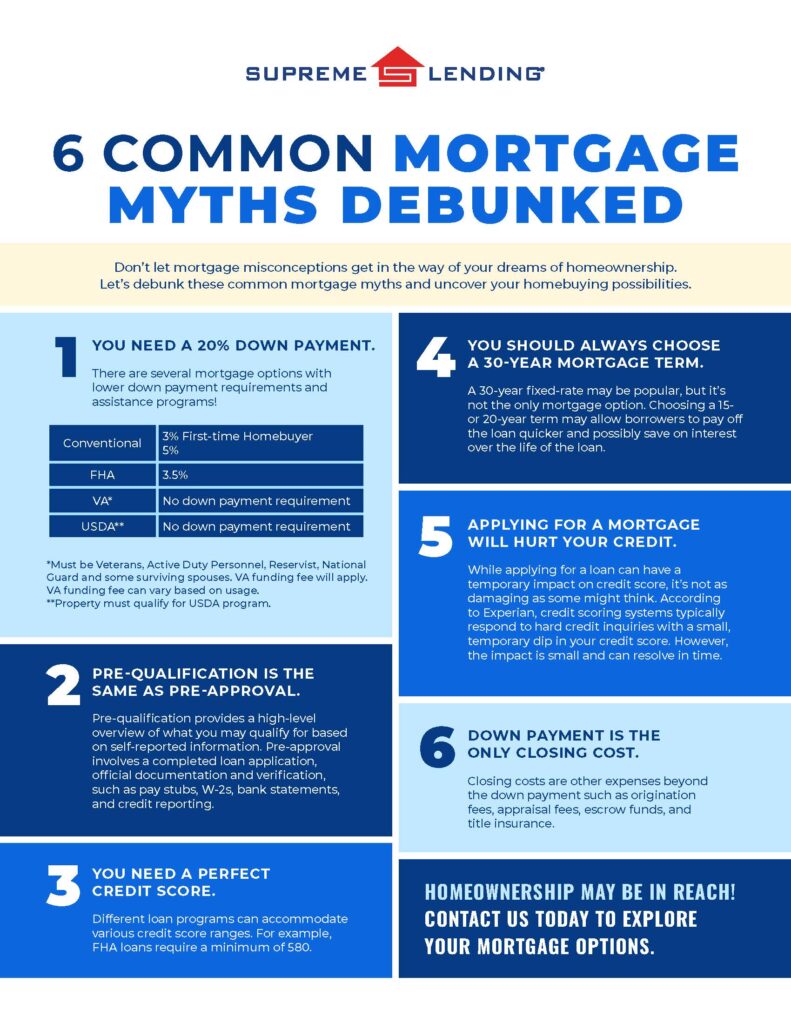

Don’t let mortgage myths get in the way of your dreams of homeownership. Unfortunately, there are several misconceptions about home financing that can make getting approved for a loan seem more difficult than it could be. Supreme Lending is here to set the record straight and help you navigate the steps of the mortgage process with the knowledge you need. Let’s debunk these six common mortgage myths and uncover your homebuying possibilities.

#1 Myth: You Need a 20% Down Payment.

Believing that you must have at least a 20% down payment saved up for a home may be one of the most common mortgage myths of all. When in fact, there are several loan options with lower down payment requirements.

For example, Conventional loans can require as low as 3% down for first-time homebuyers and 5% for repeat buyers. FHA loans require 3.5% down, serving as another affordable option. VA* and USDA** loans are unique in that they require zero down payment. There are also several down payment assistance programs for eligible homebuyers depending on various factors such as income or geographic location.

Why 20% Down?

The 20% myth may be misunderstood because of private mortgage insurance (PMI). If you don’t put down 20% for a Conventional loan, lenders will typically require you to have PMI, which is an added cost to your monthly mortgage payment. It’s important to note that if a borrower reaches a specified equity threshold in their home, mortgage insurance may be removed.

#2 Myth: Pre-Qualification Is the Same as Pre-Approval.

Nope. These terms are often used interchangeably but they are not the same when it comes to where you are in the loan process. Both provide an estimate of how much you may be able to afford for your monthly mortgage payments. However, the key difference between a mortgage pre-qualification and pre-approval is how lenders verify your information.

Pre-qualification is a high-level mortgage estimate based on self-reported information, such as income, debts, and assets. Plus, it’s oftentimes quicker to obtain.

On the other hand, a pre-approval takes a more detailed approach. This involves a completed loan application. Homebuyers must provide thorough documentation of financial history such as pay stubs, W-2s, and bank statements for verification. To get pre-approved, lenders will also verify your credit and employment.

#3 Myth: You Need a Perfect Credit Score.

A recent study found that people either don’t know or significantly overestimate the minimum credit score required for a typical mortgage, reported by Mortgage Professional America. While a higher credit score may help you secure more favorable mortgage rates or qualify for a higher loan amount, you don’t need to have flawless credit.

Different loan programs can accommodate various credit score ranges. For example, FHA loans are designed to make homeownership more accessible by accepting lower credit scores, a minimum requirement of 580.

#4 Myth: You Should Always Choose a 30-Year Mortgage Term.

A 30-year fixed-rate may be one of the most popular mortgages, but it’s not the only one to choose from. Depending on your situation or long-term goals, other mortgage terms may be a better fit. Whether it’s a 15-year term to pay the loan off quicker, or a 20-year term, Supreme Lending offers a wide range of options that can be tailored to match your needs.

#5 Myth: Applying for a Mortgage Will Hurt Your Credit.

While applying for a loan can have a temporary impact on your credit score, it’s not as damaging as some might think. When you apply for a new loan, lenders will pull your credit. This is also known has a hard inquiry for your credit report. According to Experian, credit scoring systems typically respond to hard credit inquiries with a slight, temporary dip in your credit score by a few points. However, the impact is small and can resolve in time.

Additionally, once approved for a mortgage, making on-time monthly payments may strengthen your credit in the long run.

#6 Myth: Down Payment Is the Only Closing Cost.

The down payment is a key part of closing a loan but isn’t the only cash you need to finalize your mortgage. Closing costs are other expenses beyond the down payment such as origination fees, appraisal fees, escrow funds, and title insurance. These costs will be outlined in the closing disclosure.

In addition, some lender programs allow borrowers to buy discount points to reduce their interest rate. This is essentially buying down the rate to save in interest over time. One discount point would equal 1% of the loan amount and would be included as a closing cost.

Understanding the Mortgage Process

Buying a home is one of the most significant purchases you can make. It’s crucial you’re properly informed about the loan process. By debunking these common mortgage myths, we hope to empower you with the knowledge needed to make informed decisions.

At Supreme Lending, we’re dedicated to providing personalized service and expert guidance throughout your homebuying journey. If you have any questions or want to explore your mortgage options, contact us today!

*Must be eligible Veterans, Active Duty Personnel, Reservist, National Guard, or qualifying surviving spouses. VA funding fee will apply. VA funding fee can vary based on usage.

**Property must qualify for USDA program.

by SupremeLending | Jul 18, 2024

When it comes to securing a mortgage, a key factor that lenders consider when evaluating a borrower’s lending capacity is Loan-to-Value (LTV) ratio. Understanding mortgage LTV, how it’s calculated, and how it can impact your mortgage can help you make informed decisions during the homebuying process. Let’s dive into the details of LTV ratios and why they matter.

What Is Loan-to-Value (LTV) Ratio?

The LTV ratio is a financial term used by lenders to assess the risk of a loan. It compares the loan amount to the appraised value of the property being purchased or refinanced.* The LTV ratio is expressed as a percentage, demonstrating how much of the property’s value is being financed through the mortgage.

*By refinancing an existing loan, total finance charges may be higher over the life of the loan.

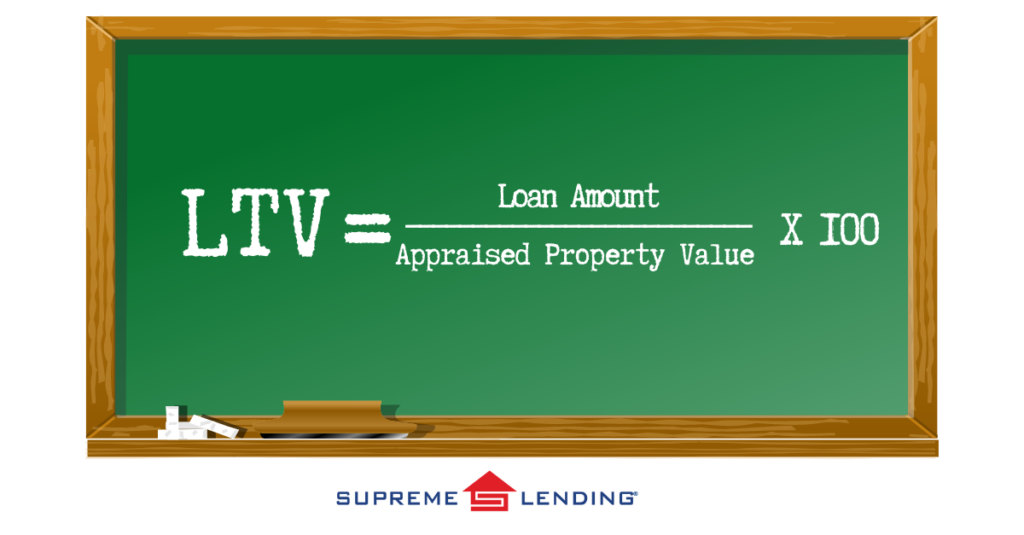

How Is Mortgage LTV Calculated?

The LTV ratio is calculated using the following formula:

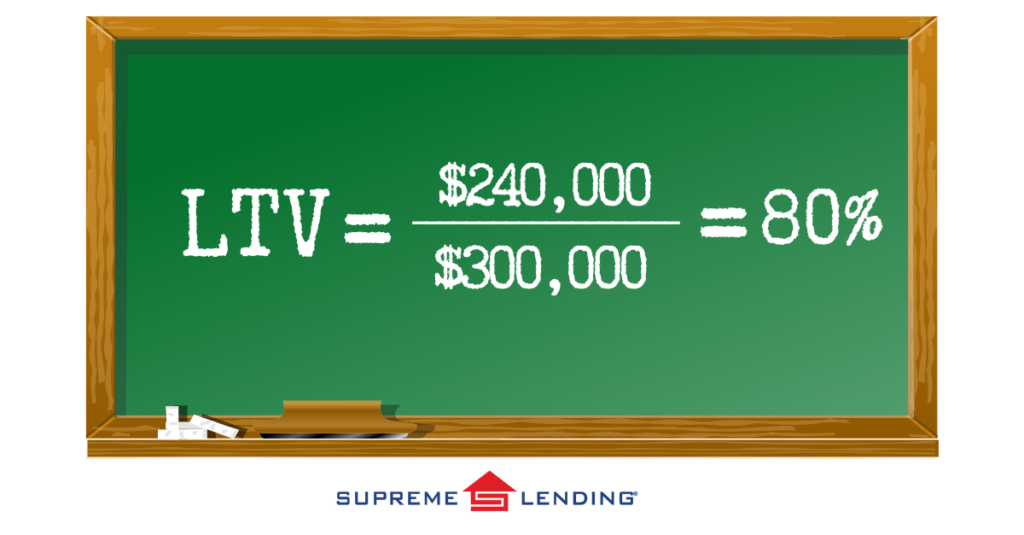

For example, if you’re purchasing a home with an appraised value of $300,000, and you’re borrowing $240,000, the mortgage LTV would be 80%:

How LTV Relates to Mortgage and Homebuying

LTV ratios play a crucial role in the mortgage approval process. Lenders use LTV to determine the level of risk associated with a loan. A lower LTV signifies lower risk, as the borrower has more equity in the property. Consequently, a higher LTV indicates higher risk for the lender, as the borrower has less equity.

How to Measure Mortgage LTV Ratios

A fair LTV ratio is typically 80% or lower. An LTV ratio of 80% or less is favorable because it often means the borrower is not required to pay for private mortgage insurance (PMI), which is usually mandatory for higher LTV ratios. PMI protects the lender in case of default but adds extra cost for the borrower.

LTV Requirements by Common Loan Types

Loan-to-Value criteria depends on the type of loan. Here’s a breakdown of common LTV limits to keep in mind:

- Conventional Loans:

- Maximum LTV: 80% to avoid PMI

- With PMI: Up to 97%

- FHA Loans:

- Maximum LTV: 96.5% for borrowers with a credit score of 580+

- VA Loans:

- Maximum LTV: 100% (no down payment required for eligible Veterans)

- USDA Loans:

- Maximum LTV: 100% (no down payment required for eligible rural properties)

Frequently Asked Questions About LTV Ratios

How Can I Lower My LTV?

You can lower your LTV ratio by making a larger down payment or by choosing a less expensive property relative to the loan amount.

Does a High LTV Affect the Mortgage Interest Rate?

Yes, a higher LTV ratio may result in higher rates because it can be seen as a higher risk for the lender. On the other hand, a lower LTV may qualify for lower rates.

What If My LTV is Above 80%?

If your LTV ratio is more than 80%, you may be required to pay mortgage insurance. This adds protection for the lender and an additional cost to the monthly mortgage payment.

Can LTV Ratios Change?

Yes, Loan-to-Value ratios can change over time as you pay down your loan and as the value of your property increases.

Understanding mortgage LTV is important to making informed decisions about your home financing. By knowing how your Loan-to-Value is calculated and its impact toward your mortgage, you can better navigate the homebuying process and know what to expect.

Our experienced and knowledgeable team at Supreme Lending is committed to helping you achieve your dream of homeownership with confidence and ease. Contact us today to learn more about your loan options and get pre-qualified today.

Related article: Mortgage DTI: What Is Debt-to-Income Ratio?

by SupremeLending | Jul 8, 2024

Learn about Supreme Lending’s BEYOND Program, an ITIN Loan Option.

Did you or someone you know just miss out on becoming eligible for a mortgage? Supreme Lending may have the solution with the BEYOND mortgage program, commonly known for being an ITIN loan option. However, it’s so much more than that!

Whether a gig worker, recent college graduate, or multi-generational family, the BEYOND program provides more opportunities for prospective homebuyers who may not yet qualify for an FHA loan. What is the BEYOND mortgage program, who can benefit from it, and how does it work? Read on to discover if this loan option could unlock the door to homeownership.

What Is Supreme Lending’s BEYOND Loan Program?

Essentially, the BEYOND program offers a lower down payment option for homebuyers who may be just beyond eligibility for an FHA loan, including non-permanent resident aliens with an Individual Taxpayer Identification Number (ITIN) or U.S. citizens and individuals who don’t have an established work or tax history.

Through this program, eligible borrowers can buy a primary residence with a purchase sales agreement. Then, they can refinance* down the road into direct ownership if they meet the qualifications in the future. This allows borrowers to get mortgage-ready while holding the equitable title interest.

Who Is the BEYOND Program Designed for?

Supreme Lending’s BEYOND program may be a good ITIN loan option for foreign national borrowers who do not have work authorization or a Social Security Number (SSN). However, ITIN borrowers are not the only people who may benefit from this unique loan program. Gig workers who may not have an established W2 income or newly self-employed people may qualify. Here’s an overview of borrowers who may be eligible for this program:

- Non-permanent resident aliens with an Individual Taxpayer Identification Number (ITIN); no work authorization or SSN required

- For example, ITIN mortgages typically require a higher down payment of 10-20%, so this program offers a more affordable ITIN loan option

- Deferred Action for Childhood Arrivals (DACA)

- 1099 or gig workers

- Borrowers who are relocating or awaiting citizenship

- Borrowers with a new job

- College graduates; deferred student loans do not need to be included in Debt-to-Income (DTI) ratio

- Multi-generational households

- Borrowers with credit issues preventing mortgage approval

How It Works?

- The first step of the BEYOND program is simply determining if the homebuyer qualifies. They will need to meet the program guidelines and get pre-approved for the purchase price limit based on income qualifications. An important starting point is to determine if the borrower has proof of successfully making rental payments within the last year. Several other criteria will also need to be considered.

- Once approved and the buyer makes an offer to buy a qualified property, they’ll enter into a sales contract. The contact is then assigned to a third-party government entity approved by the U.S. Department of Housing and Urban Development (HUD) to purchase the home as an investment.

- The buyer must pay at least a 3.5% down payment along with additional administrative fees.

- An FHA appraisal and home inspection are required.

- The government entity buys the home using an FHA loan.

- The homebuyer also signs a seller-financing agreement with the third-party entity, which gives them a recorded equity interest in the property. This agreement acts similar to a standard mortgage or deed of trust.

BEYOND Loan FAQs

What Proof of Rental History Is Accepted?

A key requirement is for the borrower to provide proof of successfully paying rent for the past year. This could be through checks, money orders, or reviewing bank statements. Living for free with family members will not qualify.

Are There Credit Requirements?

For ITIN borrowers, no credit score is required. For non-ITIN borrowers, a minimum credit score of 600 is required.

What Form of Identification Is Needed?

The borrower will need to present two forms of unexpired government-issued identification. One must be a picture ID (i.e. driver’s license or passport). ITIN borrowers must provide proof of ITIN documentation. Valid IDs from other countries are accepted.

What Upfront Costs Are Required?

Qualified borrowers will need to pay at least the minimum down payment of 3.5% along with program administration fees and the first monthly payment.

Does the Borrower Own the House?

They will have equitable title interest, which is legal ownership. This means borrowers can benefit from any equity gains. However, the title of the home hasn’t been fully transferred. Additionally, for borrowers who do qualify on their own in the future, the loan may be refinanced* into the borrower’s name and have the title transferred.

Homeownership In Reach

With programs like BEYOND, Supreme Lending is committed to providing affordable, flexible mortgages for all. Contact your local branch to see if you may qualify and take the leap into homeownership.

*By refinancing an existing loan, total finance charges may be higher over the life of the loan.

by SupremeLending | Jun 26, 2024

Understanding Down Payment Assistance Programs

When it comes to buying a home, one of the most common misunderstandings is that you need at least a 20% down payment. This misconception can discourage potential buyers, especially first-time homebuyers, from pursuing their dream of homeownership. Good news – there are several low and no down payment options, including down payment assistance programs, designed to help people become homeowners without hefty upfront costs. Discover what down payment assistance is, how it works, benefits, and other lower down payment mortgage options.

What Are Down Payment Assistance Programs?

Down payment assistance (DPA) refers to programs designed to provide financial aid to help cover part or all of the down payment and, in some cases, closing costs associated with purchasing a home. These programs can significantly reduce the upfront costs of buying a home and help more people across the country buy a home.

How Does Down Payment Assistance Work?

Down payment assistance programs are often provided by state and local governments, non-profit organizations, or other entities dedicated to promoting homeownership in local communities. DPA can come in various forms, such as grants, forgivable second loans, deferred payment loans, and tax credits. Down payment assistance programs can have specific guidelines, often targeted for first-time homebuyers and lower income areas.

- Grants. These are funds that do not need to be repaid. Essentially, they are a gift to help cover a home’s down payment.

- Forgivable Loans. When a loan is forgivable, a borrower doesn’t need to repay it after a certain time period and agreed upon criteria is met. For example, living in the primary home for a set number of years.

- Deferred Payment. This refers to loans that do not need to be repaid until the home is sold, the borrower refinances, or the mortgage is paid off.

- Tax Credits. Some down payment assistance programs offer mortgage credit certificates (MCCs) that provide a direct tax credit based on the interest paid on the loan.

Common Eligibility Requirements

While loans and down payment assistance vary by lenders and program guidelines, here’s an overview of some general eligibility criteria that may be considered.

- Income Limits. Many mortgage DPA programs have maximum income limits based on family size and location. Some lenders may consider how a borrower compares to the Area Median Income (AMI).

- Credit Score. Like most mortgages, credit score is a major factor. A minimum credit score is typically required, such as 620 for FHA and VA.

- First-time Homebuyers. Several down payment assistance programs are designed specifically for first-time homebuyers or people who haven’t owned a home within the past three years. Homebuyer education may also be included with the program as well.

- Primary Residence. In general, down payment assistance is used toward owner-occupied primary residences.

- Location. Properties may also need to be in a specific geographic area or within a targeted zone for revitalization to qualify.

- Profession. Some down payment assistance programs may also target specific occupations, such as first responders, educators, or healthcare providers. These options help give back to those who serve our communities.

Benefits of Down Payment Assistance

- Affordability. Evidently, down payment assistance can greatly reduce the amount of upfront costs when buying a home. When getting pre-qualified for a DPA program, you’ll be able to determine the right programs and potential savings.

- Increased Accessibility. Many people who might not have qualified for a traditional mortgage due to lack of savings, may qualify using down payment assistance. This helps open more doors to homeownership in your community.

- Flexibility. Down payment assistance typically can be combined with various loan types, including FHA, VA, and USDA. These typically already have lower down payment requirements to begin with. Work with an experienced, knowledgeable loan officer to discuss your options and understand what you may qualify for.

Types of Assistance

Local and State Bond Programs

Many local, regional, and state governments offer down payment assistance programs. Supreme Lending is proud to partner with these types of organizations to provide a wide range of DPA options across the country. Examples include statewide programs through the Texas State Affordable Housing Corporation (TSAHC) or California Housing Financing Agency (CalHFA), and more localized options, such as the Orange County Housing Finance Authority’s First-Time Homebuyer program.

Specialized Options

Fannie Mae and Freddie Mac also have down payment assistance options, such as HomeReady® and Home Possible® that offer down payment requirements as low as 3% for Conventional loans.

Supreme Lending’s Down Payment Assistance

Through Supreme Lending’s Supreme Dream 100% financing, no-money-down program, qualified borrowers get a 30-year fixed FHA loan, followed by a fully forgivable second loan to be used toward down payment, closing costs, and pre-paids. A unique feature of this program is that no income limits are required and it can be combined with a 2-1 temporary rate buydown.

Other Low Down Payment Mortgages to Consider

- FHA loans can require down payments as low as 3.5%.

- VA loans offer qualified military Veterans 100% financing, meaning zero down payment required.

- USDA loans, guaranteed by the U.S. Department of Agriculture, offer a zero down payment requirement for properties in eligible rural areas.

- Click here for an overview of common down payment requirements broken down by mortgage type.

At Supreme Lending, we’re always looking for innovative ways to help make homeownership more affordable. Whether it’s through local bond programs, low down payment loans, or our own Supreme Dream down payment assistance.

Contact us today to explore your mortgage options and down payment assistance programs.

by SupremeLending | Jun 20, 2024

Ease into a Mortgage with a Temporary Interest Rate Buydown

In today’s mortgage market, finding ways to make homeownership more affordable is key. One effective option is a temporary rate buydown mortgage. What is a rate buydown and how can it benefit borrowers? Let’s explore how a mortgage buydown works, types of buydowns, and unique advantages of these programs – especially in higher interest rate environments. Plus, learn how Supreme Lending offers a variety of buydown options to fit unique mortgage needs, including the possibility of combining down payment assistance with a temporary rate buydown, offering more affordability for first-home homebuyers.

How Does a Temporary Rate Buydown Mortgage Work?

A temporary rate buydown mortgage allows borrowers to reduce their monthly mortgage payment with a lower interest rate for a specific period of time, generally the first one to three years of the loan term. This means lower monthly payments during the agreed upon years of the mortgage. The cost difference is covered by an upfront lump sum, typically paid by the seller, builder, or lender at closing. A portion of the funds is released from an escrow account each month to cover the interest difference.

As the name suggests, these buydowns are temporary. After the buydown period ends, the mortgage interest rate resets to the original, higher rate for the remainder of the loan term.

Types of Rate Buydowns

Temporary rate buydowns can be applied to a variety of mortgage types including Conventional, FHA, and VA loans. Additionally, there are different buydown options depending on the program and duration of the initial rate buydown.

1-Year Buydown (1-0 Buydown)

- In the first year, the interest rate is reduced by 1%.

- From the second year onward, the interest rate reverts to the original note rate.

- This option may be ideal for buyers expecting their income to increase in the near future.

2-Year Buydown (2-1 Buydown)

- In the first year, the interest rate is reduced by 2%.

- In the second year, the rate is reduced by 1%.

- From the third year onward, the interest rate reverts to the original note rate.

- This provides a more extended period of lower monthly payments, allowing more time to adjust to the higher rate.

3-Year Buydown (3-2-1 Buydown)

- In the first year the interest rate is reduced by 3%.

- In the second year, the rate is reduced by 2%.

- In the third year, the rate is reduced by 1%.

- From the fourth year onward, the rate reverts to the original note rate.

- This offers the longest period of reduced payments for affordable financing.

Benefits of Buydowns in a Higher Rate Market

Lower Initial Payments

The primary benefit of a temporary rate buydown mortgage is lower monthly payments during the early years of the loan. This can be especially beneficial in a higher-rate market, making homeownership more accessible.

Financial Flexibility

Lower initial payments can provide the flexibility needed to handle other expenses associated with purchasing a home, such as relocating costs, furnishing the new home, or making home renovations or repairs.

Gradual Adjustment

A buydown allows borrowers to ease into the full mortgage payment gradually, giving them time to adjust their budget and plan accordingly.

Possibility to Refinance* If Rates Drop

Temporary rate buydown mortgages are a great option to provide lower initial monthly payments during the specified buydown period. After that, if interest rates drop below the original note rate, the borrower may have the option to refinance to a lower rate. This may save costs in interest over the life of the loan.

*By refinancing an existing loan, total finance charges may be higher over the life of the loan.

Supreme Lending’s Buydown Options

Supreme Lending is proud to offer several buydown options to suit individual mortgage needs. Our experienced mortgage professionals can help you explore 1-year, 2-year, and 3-year buydown programs to see if this option is right for you. We may also be able to apply a temporary rate buydown with our Supreme Dream Down Payment Assistance program, making homeownership even more accessible. This combination may significantly reduce upfront costs and monthly payments in the early years of the mortgage.

To learn more about temporary rate buydown mortgages and other home financing options, contact Supreme Lending today.