by First Integrity Team Supreme Lending | Jan 11, 2025

An Overview of Your Mortgage Checklist

Ready to buy a home but don’t know where to start? We’ve got you covered with what is needed for the loan application process with this basic mortgage checklist! To qualify for a home loan, lenders will need to review several personal and financial documents during the application and mortgage underwriting process. To help streamline the process, it’s helpful to know what all you may need to provide to ensure your mortgage goes smoothly. Once you have completed the loan application and given your intent to proceed with your loan, here’s a general mortgage checklist of required documentation.

Proof of Income

Lenders need to verify that you have a steady income to make your mortgage payments. This is a key part of the loan process, and the documents you’ll need to provide include:

- Pay stubs from the last 30 days (most current)

- W-2s and tax returns from the last two years

Employment Verification

In addition to proof of income, lenders verify your employment to ensure you have stable job security. Be prepared to provide:

- Employment history for the last two years, address any gaps

- Offer letter or contract if you’ve recently started a new job

Credit History

Your credit score plays a big role in determining what loan options and rates you may qualify for. Lenders will pull your credit report to review your creditworthiness. You have options to review your credit beforehand as well.

Proof of Assets

To help determine how much you may be able to afford for a down payment and closing costs, lenders will review your financial assets. At this point in the process, the following will be needed.

- Bank statements from the last two months

- Investment account statements including 401(K), IRAs, stocks, CDs, money market funds, Terms of Withdrawal Retirement, profit share, etc.

- Source of any large deposits, for example if you received mortgage gift funds or sold a large asset

Additionally, any assets used for a down payment, closing costs, and cash reserves must be documented by a paper trail.

Debt-to-Income Ratio

Lenders will review your debt-to-income, known as mortgage DTI, to ensure you can handle additional mortgage payments. This is calculated using:

- Total monthly debt payments, for example credit cards, car loans, student debt

- Monthly gross income including salary, investment income, bonuses, and commissions

Identification

To confirm your identity, you’ll need to provide:

- Government-issued I.D. (valid driver’s license or passport)

- Copy of Social Security card (SSN)

- Residency history, typically for the last two years including landlord information for renters or a mortgage statement if applicable

Other Information Depending on Your Situation

In addition, you may need to provide other documentation depending on your current circumstances.

These could be:

- If paid off a mortgage in last year, need copies of the release of mortgage lien

- If own 25% or more of business, need company tax returns for last two years

- Divorce decree or child support order, if applicable

- Refinance copy of note, Closing Disclosure, and survey

- Relocation Agreement if the move if financed by employer (i.e. buyout agreement, documentation outlining company-paid closing cost benefits)

- Insurance quote

Program-Specific Documents

For government-insured loan programs, there are a few more items you’ll be required to provide:

- FHA: Copy of Social Security card for each applicant and co-applicant

- VA: Original Certificate of Eligibility (COE), copy of DD214 discharge paper, and contact information of nearest living relative

- FHA and USDA: Total household income of all borrowers moving into the new home

Preparing for a Smooth Process

By preparing yourself for a seamless mortgage process, you’re showing lenders you’re organized and ready to move forward. This preparation may help prevent potential delays, reduce stress, and have the majority of items needed to secure your dream home. Bookmark this mortgage checklist to have on-hand when you’re ready to start your homebuying journey.

If you have any questions about what documents are needed or how to get pre-qualified, our team at Supreme Lending is ready to help!

Related Articles:

by First Integrity Team Supreme Lending | Jan 9, 2025

All You Need to Know About the FHA 203(h) Disaster Relief Loan Program

When natural disaster strikes, the devastation it leaves behind can be overwhelming, especially if your home is damaged or destroyed. At Supreme Lending, we know how difficult it can be to rebuild after such destruction. That’s where the FHA 203(h) Disaster Relief Loan may be able to help as an affordable option for those in eligible areas.

If you’ve been affected by disaster and are looking to rebuild or purchase a new home for a fresh start, Supreme Lending is here to help you navigate the challenging time with care and expertise. This guide will walk you through the FHA 203(h) loan, how it works, benefits, and why it may be a valuable program for helping disaster victims get back on their feet.

What Is the FHA 203(h) Disaster Relief Loan?

The FHA 203(h) is a government-insured mortgage program that provides financial assistance to individuals whose homes have been damaged or destroyed in federally declared disaster areas. This is designed to help homeowners and renters alike rebuild or purchase new homes in the wake of devastating events like hurricanes, floods, tornadoes, and wildfires.

What makes the FHA 203(h) Disaster Relief Loan unique is the ability to help make homeownership more attainable after such tragedy by offering flexible guidelines and 100% financing.

How Does FHA 203(h) Work?

The FHA 203(h) Disaster Relief Loan works similarly to other FHA programs but comes with added benefits and provisions specifically for disaster victims. Here’s a breakdown of how it works.

What Properties Are Eligible?

To qualify, your current home must be in a Presidentially Declared Major Disaster Area (PDMDA) and must have been damaged to the point where it is no longer livable. The loan must be secured within one year of the disaster declaration, offering you plenty of time to regroup and take the next step towards recovery.

Program Benefits

- No down payment required. One of the biggest benefits of this program is that there is no down payment requirement for eligible borrowers. This makes it easier to secure financing without the burden of saving for large upfront costs, especially after facing potential hardships caused by a disaster.

- Minimum credit score of 580. While there are still credit parameters in place, the FHA 203(h) offers more lenient requirements than other financing options. This may help borrowers whose credit was negatively impacted due to the natural disaster.

- Available for single-family or FHA-approved condos. The home must be a primary residence – either a single-family home or approved condominium project. This program is not designed for second homes or investment properties but is focused on truly helping homeowners get back on their feet.

- Purchase location flexibility. Through this program, it allows you to purchase a new home anywhere in the United States. The replacement home doesn’t have to be in a designated disaster area.

Combining FHA 203(h) with 203(k) Renovation

The FHA 203(h) program also offers the option to combine with an FHA 203(k) Standard or Limited Renovation loan. This involves adding renovation costs into a single mortgage to cover repairs and remodel projects ranging from minor updates to structural if approved. Plus, the damaged property is eligible regardless of the age of the home. It only needs to have been a habitable residence prior to the disaster.

Ready to Relocate or Rebuild?

Supreme Lending is here to help you move forward and rebuild when disaster strikes. To learn more about the FHA 203(h) Disaster Relief Loan or to go over other mortgage options, contact your local Supreme Lending branch today!

More Resources from the U.S. Department of Housing and Urban Development:

Related Articles:

by First Integrity Team Supreme Lending | Oct 17, 2024

Discover the Program Highlights of an FHA 203(k) Renovation Loan

Are you ready to turn a fixer-upper into your dream home? Whether it’s a home you’ve just bought or already own, renovation loans like the FHA 203(k) program may help you finance both the purchase and necessary repairs or updates all in one mortgage. Plus, the U.S. Department of Housing and Urban Development (HUD) announced that it is increasing the loan amount for Limited FHA 203(k) loans to $75,000 on all FHA case numbers effective November 4, 2024—that’s up from $35,000 which is huge news!

Here’s an in-depth look at how the FHA 203(k) renovation loan works, the differences between the Limited and Standard options, and what types of renovations may be covered.

What Is an FHA 203(k) Loan?

Insured by the Federal Housing Administration, the FHA 203(k) renovation loan allows homeowners to finance the cost of both the property and its renovations in a single loan. Whether you’re purchasing a home that needs updates or making repairs to your current home, this loan program may help make those dreams a reality. It offers the similar benefits of FHA loans for first-time buyers and repeat buyers alike. To qualify, eligible borrowers only need 3.5% down payment and there’s more lenient credit score requirements than other renovation loans.

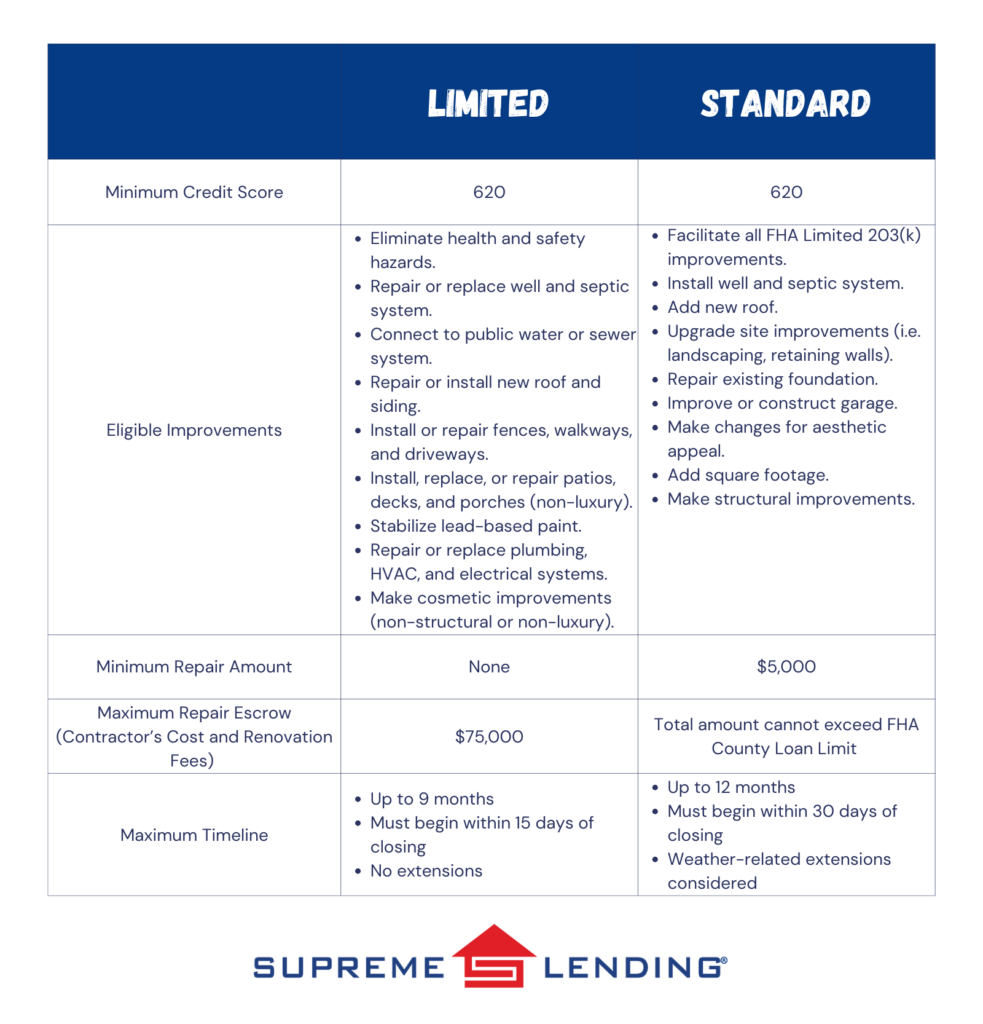

Limited vs. Standard FHA 203(k) Renovation Loan

There are two types of FHA 203(k) loans—Standard and Limited. Each has specific uses and limits depending on the scope of renovations you can make.

Limited FHA 203(k) Loan

The Limited 203(k) option is commonly used for smaller repairs and cosmetic upgrades. As mentioned, the loan amount will increase to $75,000 in November 2024, an exciting enhancement that will help open the door to renovations for more people. This loan covers non-structural projects such as remodeling kitchen fixtures, replacing flooring, painting, and minor landscaping. Unlike the Standard, the Limited program doesn’t require working with an HUD consultant or have a minimum loan amount.

Common Projects the Limited Covers

- Minor remodeling (i.e. updating kitchens or bathrooms)

- Replacing appliances or flooring

- Repainting or refinishing surfaces

- Energy-efficient improvements (i.e. installing new windows or insulation)

- Repairing roofs and gutters

Standard FHA 203(k) Loan

The Standard FHA 203(k) Renovation loan is more ideal for homes needing larger renovations and structural repairs. These may include adding rooms, replacing outdated plumbing or electrical systems, and fixing major structural issues. It has a minimum of $5,000 that must be used for renovations and the total loan amount must be within the FHA County Loan Limit. Because these projects are typically more complex, you’re required to work with an HUD-approved consultant.

Common Projects the Standard Covers

- Structural repairs or additions (i.e. adding on square footage or fixing foundation issues)

- Major systems replacements (i.e. plumbing, electrical, or HVAC systems)

- Roof repairs or replacements

- Modernization and improvements to the home’s function

- Accessibility improvements for people with disabilities

How Does the FHA 203(k) Renovation Loan Work?

The process for applying for an FHA 203(k) loan is similar to a regular FHA mortgage but comes with a few additional steps. Here’s an overview of how this loan program works.

- Find a property. Whether it’s a home you already own and want to refinance* or one you’re planning to purchase, identify a property that needs renovations.

- Get an appraisal. The home appraisal will assess both the home’s current market value as well as it’s “as-completed” value after the renovations are completed.

- Contractor and Estimates. Work with a licensed contractor to obtain the estimated costs for the repairs and improvements.

- Loan Application. You’ll apply for the loan based on the combined cost of the home and repairs.

- Renovation Timeline. Once the loan is approved, the renovation funds are placed into an escrow account and work begins. The renovation timeline can typically range from six months to one year.

*By refinancing an existing loan, total finance charges may be higher over the life of the loan.

FHA 203(k) Combined with FHA 203(h) Disaster Relief Loan

Did you know that eligible borrowers affected by federally declared disaster areas may be able to combine the FHA 203(k) renovation loan with the FHA 203(h) disaster relief loan? This means adding the renovation costs into a new mortgage if your home was destroyed and deemed unlivable. Plus, the damaged property is eligible regardless of the age of the home. It only needs to have been a habitable residence prior to the disaster.

Ready to Rebuild?

At Supreme Lending, we understand how important it is to transform a home into one that truly meets your needs. Whether you’re fixing up a new property or renovating your current home, the FHA 203(k) renovation loan offers an excellent way to finance those improvements. We’re proud to offer both Standard and Limited options to fit the scope of your home projects.

Want to learn more about FHA 203(k) renovation loans or other mortgage options? Contact our team at Supreme Lending today and get pre-qualified!

Looking for other renovation loan options? Read more:

by First Integrity Team Supreme Lending | Oct 1, 2024

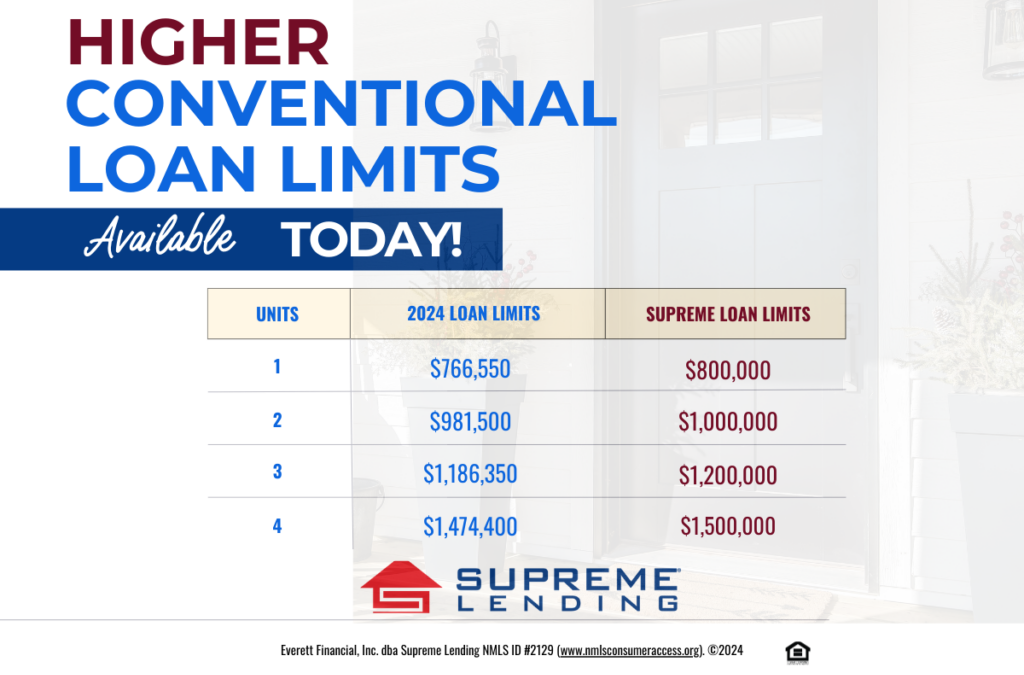

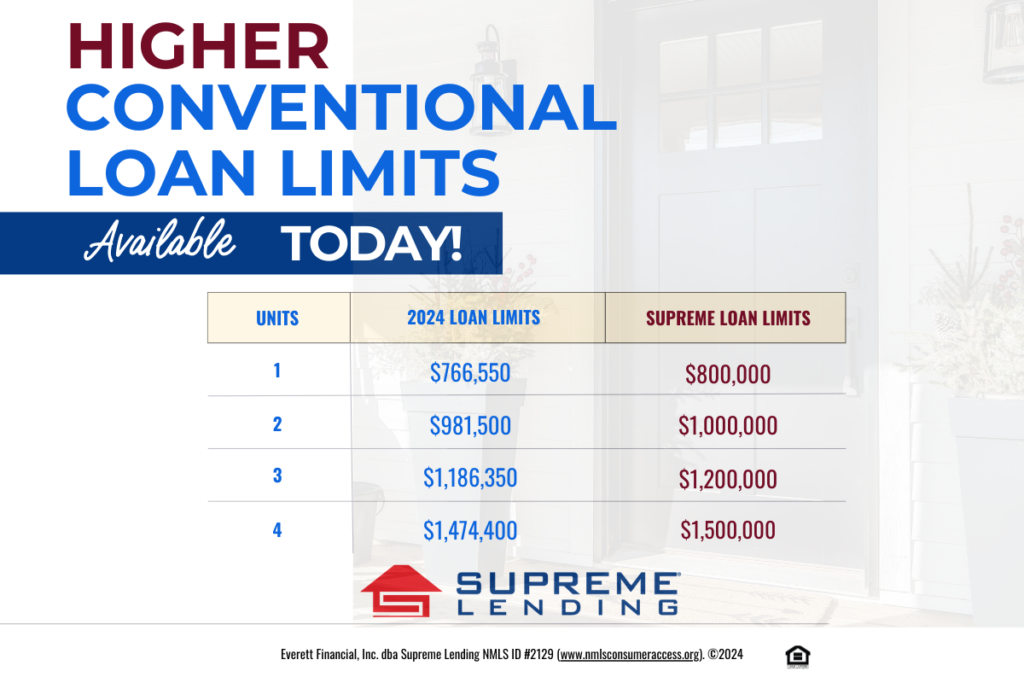

Supreme Lending is proud to announce the conforming 2025 loan limits have increased and, the best part, the company is offering the raised loan limits today. For single unit properties, the conforming limit is now $800,000, up from $766,550.

While Fannie Mae and Freddie Mac will not officially announce the 2025 conventional loan limits until the end of November, we’re pleased to honor these new limits now – empowering more people to achieve homeownership as home prices rise. You may not have to wait until next year to make your homeownership dreams come true!

Supreme Lending 2025 Loan Limits Available Now

- 1-unit property – $800,000

- 2-unit property – $1,000,000

- 3-unit property – $1,200,000

- 4-unit property – $1,500,000

The increase is effective on all new loan applications taken on or after Wednesday, September 25, 2024.

What Are Conforming Loan Limits?

Conforming loan limits set the maximum amount borrowers can finance their home while still qualifying for a conventional loan backed by Fannie Mae or Freddie Mac. Why does this matter? Staying within these limits may result in more favorable terms, including competitive rates, easier qualification standards, and lower down payment requirements.

What Happens When You Exceed Loan Limits?

If you need a loan higher than the conforming limits, you may consider a Jumbo loan. This is a good option for larger home purchases—especially in high-cost housing markets. Jumbo loans can typically require a higher credit score or larger down payment amount.

Ready to Get Started?

The increased conforming 2025 loan limits are designed to keep pace with rising home prices, making homeownership more attainable for borrowers looking to finance higher amounts while still benefiting from conventional loan advantages.

Whether you’re a first-time homebuyer or looking to upgrade, these new limits may open doors to more flexible financing options. If you have any questions or want to see if you qualify for the new, higher loan limits, contact us today to get started! We’re here to help guide you through the loan process every step of the way.

by First Integrity Team Supreme Lending | Sep 30, 2024

Buying a home is a major milestone, and while most prospective buyers are focused on saving for the down payment, there are additional homebuying costs to consider. From closing costs to ongoing home maintenance expenses, it’s important to understand the costs beyond the down payment. Let’s dive into those homebuying costs so you can be well prepared.

Down Payment: The First Major Cost

The down payment is often the largest upfront cost when buying a home. The down payment requirements depend on the type of loan to determine what you may qualify for.

- Conventional loans typically require at least 5% for eligible borrowers. For first-time homebuyers, the minimum requirement can be as low as 3%.

- FHA loans require as little as 3.5% down, making them a popular choice for borrowers looking for more flexible guidelines.

- VA and USDA loans offer no down payment requirement for eligible military veterans, active military, or buyers in defined rural areas.

Plus, there are several down payment assistance programs available to help more people achieve their dream of homeownership. While the down payment is a key part of purchasing a home, it’s not the only cost to keep in mind.

Closing Costs: Hidden Homebuying Fees

Beyond the down payment, closing costs are another significant upfront expense buyers must account for. These are fees and expenses necessary to finalize your home purchase and close the loan. Closing costs typically range from 2% to 6% of the home’s purchase price. Here’s a breakdown of common closing costs:

- Loan origination fee is charged by your lender for processing your mortgage.

- Appraisal fee covers the cost of having your home professionally appraised to determine its market value.

- Home inspection fee is paid to inspect the home for any necessary repairs or safety hazards.

- Title insurance and search fees ensure the property’s title is clear of any disputes or liens.

- Escrow fee is charged by the third party handling the closing process.

- Property taxes and homeowners insurance are typically prepaid for a portion of the costs at closing so they’re included in your mortgage escrow account.

Ongoing Costs of Homeownership

After closing on your mortgage, owning a home comes with ongoing expenses that many new buyers often overlook. These homebuying costs are essential to consider when planning for the long-term.

- Utilities include monthly bills such as electricity, gas, water, and internet. These are widely dependent on the size and location of your home.

- Landscaping and yard maintenance, whether you hire a service or handle it by yourself, keeping up with lawn care, tree trimming, and other outdoor maintenance can add up.

- Homeowners Association (HOA) fees are required when your property is in a community with an HOA. These fees may be monthly or annual and cover community maintenance and amenities.

- Property taxes are ongoing local government taxes based on the assessed value of your home. Property taxes may increase over time, so review your tax bills carefully.

- Homeowners and mortgage insurance are often required. Homeowners insurance helps protect the home in the event of potential damages, while mortgage insurance protects the lender in the event of a loan default.

- Ongoing maintenance and repairs will occur over time, from replacing appliances to fixing the roof or plumbing. It’s smart to set aside funds for common home upkeep expenses to avoid hidden costs surprising you.

What’s Next?

We hope these additional homebuying costs are not so hidden anymore! The journey to homeownership comes with several financial considerations beyond the down payment. By understanding these homebuying costs, you can be prepared to buy with confidence.

If you’re ready to explore your mortgage options, contact Supreme Lending today. We’re here to help guide you through the loan process and beyond.