by SupremeLending | Apr 17, 2024

House hunters who are interested in larger or more expensive homes that could exceed certain conforming loan thresholds may need to consider a Jumbo loan program. If you’re dreaming big in your homebuying journey, discover what exactly a Jumbo loan is, qualification requirements, and helpful considerations when looking into a Jumbo loan option.

What Is a Jumbo Loan?

To understand conforming loans, you first need to understand conforming loans, which have maximum loan amounts set by the Federal Housing Finance Agency (FHFA). The 2024 conforming loan limit in most of the country is $766,550, though this may vary depending on the county in which you’re looking to purchase a property. If a loan amount is larger than this, then it’s considered a Jumbo loan.

The FHFA establishes conforming loan limits to regulate the maximum size of loans that government-sponsored enterprises (GSEs) like Fannie Mae and Freddie Mac can purchase or guarantee. These limits are put in place to ensure stability and liquidity in the mortgage market and to promote affordable homeownership. Because of this, Jumbo loans present a higher risk to lenders and often have different requirements than conforming loans.

For example, down payment requirements for Jumbo loans are typically higher, around 20% or more of the loan amount. They may also require private mortgage insurance (PMI) or carry higher interest rates than conforming loans.

Differences Between Jumbo Loans and Conforming Loans

Let’s go over the direct differences in qualifications and other areas between Jumbo loans and conforming loans:

- Down payment requirements. Jumbo loans tend to have stricter minimum down payment guidelines, often 20% or more of the loan amount. Conforming loans may be as low as 3% for first-time homebuyers.

- Private mortgage insurance (PMI). Jumbo loans almost always require private mortgage insurance, whereas conforming loans typically only require it if the down payment is less than 20%.

- Interest rates. Jumbo loans often come with higher interest rates than conforming loans due to the potential of higher risk involved for lenders.

- Loan limits. The main difference between these two types of loans is the loan limit. If the amount you’re looking to borrow exceeds the FHFA’s limit for your county, it’s a Jumbo loan.

- Closing costs and fees. Finally, closing costs and fees tend to be higher for Jumbo loans than conforming loans because they’re generally more complex and involve more work for the lender.

Jumbo Loan Qualifications Overview

While these conditions can vary somewhat depending on your area and a few other factors, here are some general guidelines for homebuyers looking to qualify for a Jumbo loan:

- Credit score. Credit and related requirements are typically higher for Jumbo loans than Conventional loans. In general, there tends to be a hard credit score minimum of 660, and many lenders may even require as high as 720 or 740.

- Debt-to-income (DTI) ratio. The maximum DTI for a Jumbo loan is typically around 43%, though this can vary depending on the specific lender. This means that no more than 43% of your income should be going towards debts each month.

- Documentation. Jumbo loans typically require extensive documentation, often including tax returns, bank statements, and asset verification. This is to ensure that you’re able to afford and repay the loan and aren’t taking on more debt than you can handle.

- Cash reserves. Another important factor that lenders will look at is your cash reserves. This is the amount of money you have left over after closing on a property that can be used to make mortgage payments if necessary. Lenders typically like to see at least six months’ worth of mortgage payments in cash reserves, though this can vary.

- Appraisals. In certain cases, not just one but two appraisals may be required for a Jumbo loan. This is to ensure that the property is worth at least as much as the loan amount and is yet another way for lenders to protect themselves from taking on too much risk.

As you can see, there’s a lot to think about if you’re looking to apply for a Jumbo mortgage. Make sure you understand all the requirements and are comfortable with any potential risks.

Considerations for Jumbo Loans

Jumbo loans may not be for everyone. There are a few potential reasons why someone may want to opt out of choosing a Jumbo loan and go with another option:

- You may not actually need a Jumbo loan. If you’re interested in a larger home but don’t need to borrow more than the conforming loan limit, it may not make sense to take out a Jumbo loan because you can end up paying more in interest and fees than necessary.

- You don’t qualify. As noted above, the lending criteria for Jumbo loans is typically stricter. If you don’t think you can meet them, it’s probably not worth your time to apply.

- The interest rates are high. Jumbo loan interest rates tend to be higher than conforming loan rates, so if you’re not comfortable with that you may want to look at other options.

Why Go Jumbo?

While there are important factors to consider, Jumbo loans can still be a great option for larger home purchases—especially in high-cost housing markets. Jumbo loans give qualified borrowers access to more expensive properties, including luxury estates, high-end condos, and prestigious neighborhoods. This expands the pool of available housing options, catering to diverse preferences and lifestyles. Additionally, Jumbo loans can often come with customizable terms and features tailored to the unique needs of high-net-worth individuals or savvy investors.

For more information on Jumbo loans, or to learn about any of our mortgage services, contact your local Supreme Lending team today.

by SupremeLending | Apr 16, 2024

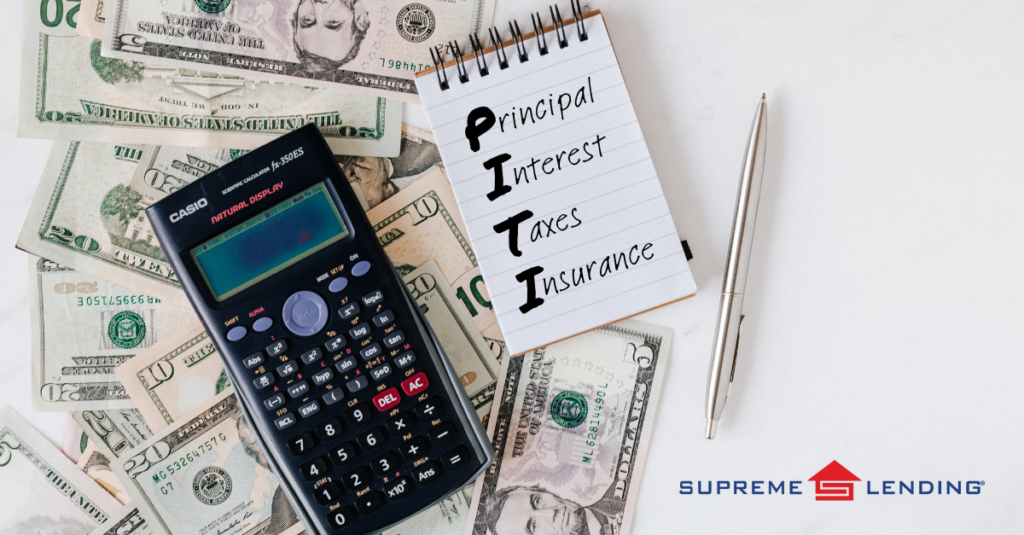

A mortgage is more than just the home loan amount, so let’s breakdown what all goes into a monthly payment beginning with the short acronym, mortgage PITI—principal, interest, taxes, and insurance. Understanding these factors can help you determine how much home you can afford and budget accordingly.

Principal (P):

Principal refers to the flat amount borrowed from a lender to purchase a home. It represents the initial loan amount, which is gradually paid down over the life of the mortgage through regular payments. Understanding the principal component of your mortgage payment is crucial for assessing the affordability of a home. A larger principal amount typically results in higher monthly mortgage payments, while a smaller principal amount may be more manageable depending on one’s budget.

Interest (I):

Interest is the rate percentage of how much you’ll pay each month as a fee for borrowing the funds. It is a fundamental component of mortgage payments. The interest rate on your mortgage directly impacts the total amount of interest paid over the life of the loan. A lower interest rate can reduce your monthly mortgage payments and lower the amount of interest you would pay over the life of the loan.

Taxes (T):

Taxes, specifically property taxes, are typically rolled into the monthly mortgage and vary by location and the appraised value of the home. These taxes fund various public services, such as schools, roads, and emergency services, within your community. Property tax rates fluctuate depending on the neighborhood and can have a significant impact on your overall housing expenses. Understanding property tax obligations associated with a prospective home is essential for accurate budgeting and planning.

Insurance (I):

Insurance, which can include both homeowners insurance and mortgage insurance, commonly have annual premiums that the lender can tie into your monthly payments. Homeowners insurance protects your investment by covering physical damages or loss to your property and belongings, such as fire, theft, or natural disasters. Mortgage insurance, which is typically required especially if you put less than 20% down, protects the lender if you default on the loan. Once you reach an agreed-upon equity threshold and loan-to-value ratio, it may be removed to lower your payments.

Practical Tips for Mortgage PITI

- Calculate Affordability. Using mortgage calculators and working with your Loan Officer can help provide an estimate for your monthly mortgage PITI payments based on your desired home price, down payment amount, interest rate, and other related terms.

- Factor in Additional Costs. In addition to PITI, consider other homeownership expenses, such as utilities, regular home maintenance, and homeowners association (HOA) fees, when establishing your housing budget.

- Build a Contingency Fund. Set aside savings for unexpected expenses or potential fluctuations in mortgage PITI payments, such as property tax increases or changes in insurance premiums.

- Reassess Periodically. Review your homeownership goals regularly and adjust as needed based on possible changes in income, expenses, interest rates, or market conditions.

Mortgage PITI—principal, interest, taxes, and insurance—serves as a fundamental framework for understanding the financial aspects of homeownership. Whether you’re a first-time homebuyer or a seasoned homeowner, examining each component of PITI offers valuable insights into how much home you can afford and helps you achieve your homeownership goals with confidence. Embrace the power of PITI as you embark on the exciting journey to owning your dream home.

Contact your local Supreme Lending branch to get started.

by SupremeLending | Apr 12, 2024

As anyone who has been through the homebuying process can tell you, there are several important documents that are typically involved. One of the single most vital, and one that all homebuyers will deal with eventually, is known as the mortgage closing disclosure.

While closing on your loan can be the most exciting step in the homebuying process, it’s important to carefully, completely review and understand what you’re agreeing to at the closing table—that’s where the official closing disclosure comes in to provide a transparent summary of all loan details. What is involved in a closing disclosure, when will it typically be sent to you, and why does it matter? Here’s everything you need to know about this important document.

Mortgage Closing Disclosure Basics

When we talk about the closing disclosure, we’re referring to a single document that lays out all the final terms and numbers associated with your mortgage so there are no surprises at the closing table, and you can close with confidence and clarity.

The closing disclosure is typically five pages in length, and includes the following details:

- Loan terms. This is where you’ll find specific information about the interest rate, monthly payments, and other important conditions of your loan agreement.

- Projected payments. Here, you’ll see a breakdown of all the different types of payments that you’ll be responsible for making over the life of the loan. This will include your principal and interest payments, as well as any taxes, insurance, or other fees that are required.

- Closing costs. All the different costs associated with acquiring and closing on your home loan will be itemized here. This can include fees for things like the appraisal, title insurance, or other third-party services.

- Transaction summary. For your reference, this section will provide a summary of all the different financial transactions that are taking place as part of your mortgage. This can include your down payment amount, as well as the total loan amount and any credits that may be applied.

- Other information. The closing disclosure may also include other helpful details about your loan, such as information about escrow accounts or potential prepayment penalties.

Timing of the Closing Disclosure

It’s required that lenders provide you with your closing disclosure no later than three days before your scheduled loan closing date. This is designed to give you sufficient time to review the document ahead of time and raise any questions or concerns that you may have. In practice, most lenders will provide the closing disclosure much earlier than this – often at least a week in advance, if not more.

Why Does the Mortgage Closing Disclosure Matter?

By now you can probably see why the closing disclosure is so important. It’s critical to review this document thoroughly before you close on your loan. This is your last chance to catch any errors or discrepancies in the loan terms or other information that’s been provided. If something doesn’t look right, be sure to bring it up with your loan officer so that it can be corrected quickly and to avoid any delays to your mortgage closing.

Even seemingly minor errors like a misspelled name or an incorrect address can cause major problems down the road. It’s always better to be safe than sorry, so take the time to review your closing disclosure carefully before you sign on the dotted line.

The closing disclosure is also key because it provides you with a clear understanding of what you’re agreeing to when you close on your loan. There’s no such thing as a “standard” mortgage, and loan terms can vary widely from one lender or loan program to the next. By reviewing your closing disclosure, you can be sure that you’re getting the loan that you agreed to, with the terms and conditions that you expected.

How to Check the Closing Disclosure

Once you receive your closing disclosure ahead of your mortgage closing date, it should immediately become one of your top priorities. As noted above, it’s crucial to ensure the details of your loan are accurate, and that all parties involved in the transaction have the proper information.

Here are some basic steps for checking your mortgage closing disclosure:

- Details first. In most cases, it’s recommended to first move through the simple details of the closing disclosure to ensure they’re correct. Check to make sure no names have been misspelled and that the address of the home being purchased is listed correctly, including the zip code. As mentioned, even small errors in areas like these can have a large trickle-down effect during closing, so it’s important to confirm them – and if they’re wrong, quickly send the disclosure back to your lender so it can be corrected.

- Loan terms. Next up, you should review the entire section on your loan terms and confirm accuracy of each detail. Make sure your monthly payment amounts match prior agreed upon documents, for instance, and that your mortgage interest rate percentage is what you expected it to be. Do not let any errors here slide through the cracks.

- Closing costs. Be sure to oversee the closing costs as well, confirming they’re accurate. For example, the document should list the precise amount you’re paying for your down payment, plus any other fees involved in the closing of the home purchase.

- Sign and submit back. Once thoroughly assessed and any issues or errors have been fixed, it’s time to sign the closing disclosure and return it to your lender, which can be done either in-person or virtually. Congratulations, you’re ready for closing day!

For more on closing disclosures within your homebuying process, or to learn about our wide variety of home loan options, contact your local Supreme Lending branch.

by SupremeLending | Apr 9, 2024

When considering buying a home and what your mortgage payment will look like, it’s important to be familiar with private mortgage insurance (PMI). All parties in the mortgage and homebuying process must be protected from certain risks, and this includes not only buyers and sellers, but also mortgage lenders. That’s where PMI comes in.

What exactly is private mortgage insurance, when is it required, what types are there, and when can it be removed? Here’s a breakdown of PMI and how it may impact your mortgage.

Private Mortgage Insurance Basics

PMI is an insurance that homebuyers are typically required to have when they pay less than 20 percent down payment for a home with a Conventional loan. The purpose of PMI is to protect the lender in case the borrower defaults on the loan and fails to make payments. This mitigates risk for the loan provider. If a property goes into foreclosure, PMI can reimburse the lender for a portion of their losses.

The cost for PMI is typically rolled into the monthly mortgage payment and funneled to the insurance provider—in the event the lender needs to make a claim.

It’s important to note that PMI is not homeowners insurance, which protects against things like fire damage or theft. PMI is required by lenders, and it only covers the lender in case of default. It’s not used to protect homebuyers’ interests. However, having PMI may allow borrowers to buy a home sooner than later, without having to save up for a larger down payment.

Types of PMI

While private mortgage insurance plans have the same goals, there are a few different ways to structure the PMI payments applied to a mortgage depending on specific circumstances or preferences. These options include:

- Buyer-Paid PMI: By far the most common type of PMI, buyer-paid private mortgage insurance involves the homebuyer or borrower paying a monthly insurance premium, which is added on to the monthly loan payment and paid to the insurance provider, though the charge can sometimes be rolled into the mortgage itself if applicable.

- Lender-Paid PMI: A much less common option is when the lender pays the monthly premiums, however as a result, the borrower would pay a higher interest rate to make up for the lender’s investment.

- Single-Premium PMI: This type of private mortgage insurance consists of the borrower paying for the full PMI policy upfront in a single lump sum, often at closing. Once this is paid, it eliminates monthly PMI payments.

- Split-Premium PMI: Borrowers may also have the option to combine the PMI payment options listed above by paying an upfront lump sum at closing that doesn’t cover the entire insurance policy, so a lower monthly premium is still required in addition to the mortgage payment.

Benefits of PMI

When lenders have the appropriate protections in place to provide loans, like requiring PMI in certain cases, they can offer mortgages to more families and individuals than if they were faced with taking on more risk.

Similar to how car insurance can protect both the owner of the car and the lender in case of an accident, private mortgage insurance is just another way to ensure that things go smoothly for all parties involved in a home loan. It gives more people the opportunity to buy homes with lower down payment options, while also making sure that lenders have protection against borrowers defaulting on their loans.

When PMI Is Required and How to Get Rid of It?

As noted above, the most common PMI requirement is when a homebuyer puts down less than 20 percent for a Conventional loan. However, this isn’t a set-in-stone rule. There can be loan programs with lower down payment requirements that may not require PMI. Always discuss with your loan officer to go over your qualified options.

Additionally, in most cases, PMI can be removed at some point during the life of the loan. Generally, once the borrower reaches 22 percent equity built in the home through things like paying down the mortgage or appreciation of the home’s value, PMI can be removed. This is done by request so if you think you may have reached this point, it’s important to contact your lender and ask about removal of the insurance. In other situations, PMI may automatically be removed once the homeowner reaches a certain agreed upon equity threshold.

For more on private mortgage insurance or to learn about other home loan programs, contact the team at Supreme Lending today.