by SupremeLending | Mar 21, 2024

Picture this – you currently own or want to buy a home with good bones, but it needs some TLC. The good news is that you don’t have to handle a home remodel alone. Renovation loans are a great option to help fund home improvements, repairs, and enhancements by rolling the renovation costs into a single mortgage payment. It’s important to understand how renovation or home improvement loans work, types of renovation loan options, and benefits.

What Is a Renovation Loan?

Renovation loans are designed to help borrowers finance home improvement projects that will increase the value of the home. Whether you’re planning a small home makeover or extensive rehab project, a renovation loan combines a traditional purchase or refinance mortgage with the cost of renovations—it is an all-in-one mortgage financing option that covers the upfront costs of large repairs and projects.

Taking on the remodel before moving in can enhance your living space and home functionalities without the pressure of taking out an additional loan or paying out of pocket for costly repairs in the future.

Types of Renovation Loans

When it comes to renovation loans, there are a few options for prospective homebuyers and homeowners to consider based on eligibility, timing, and the scale of the home improvements needed.

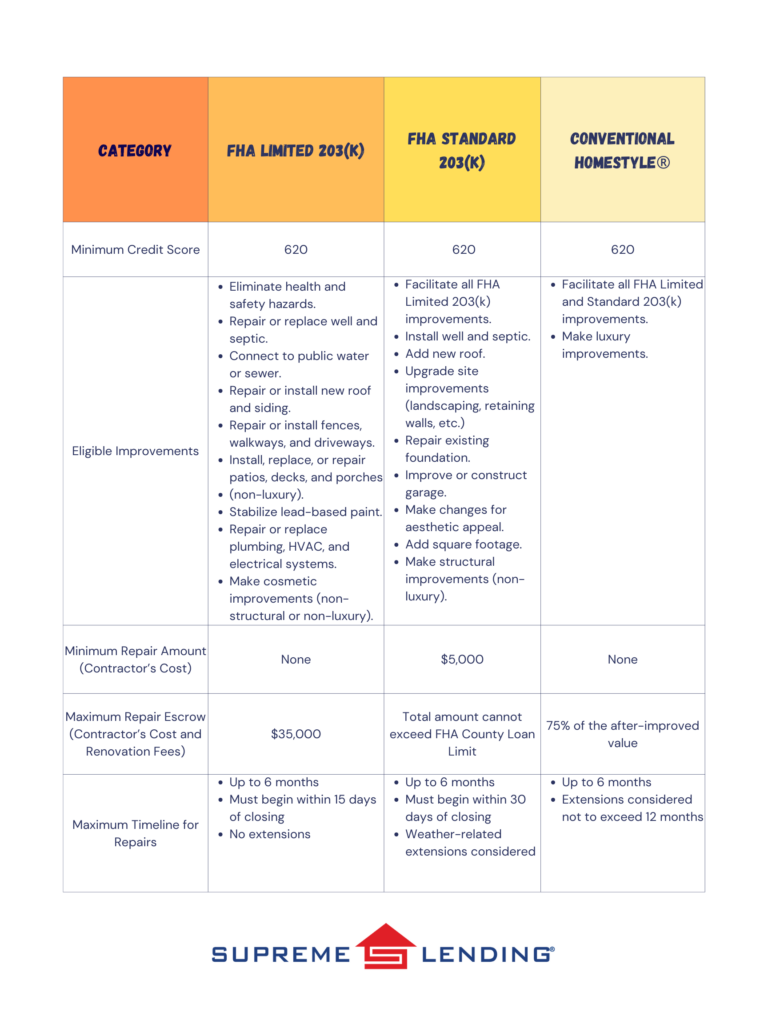

FHA 203(k) Renovation

An FHA 203(k) loan, or an FHA rehab loan, is insured by the Federal Housing Administration and provides two options depending on the scope of the home improvement projects, including Limited 203(k) and Standard 203(k), offering different levels of renovation financing.

The minimum down payment for an FHA 203(k) loan is 3.5%. An FHA 203(k) loan covers common basic home improvements and repairs but excludes larger luxury projects and amenities. The Limited option has no minimum renovation amount and can cover up to $35,000 in renovation costs. The Standard has expanded eligible improvements including some structural upgrades and a minimum renovation cost of $5,000. Typically, all renovations must be completed within 6 months.

VA Renovation

The Department of Veterans Affairs (VA) also has a Renovation loan option. A VA Renovation loan offers 100% financing for eligible U.S. Veterans or military personnel to cover a mortgage combined with planned renovation costs into a single loan. Eligible home improvements are similar to FHA 203(k) to cover common upgrades that will make the property safer, healthier, or more functional, excluding luxury projects. VA Renovation loans can finance up to $50,000 in home repair costs.

Conventional Renovation

A Conventional Renovation loan, such as Fannie Mae’s HomeStyle® program, is another financing option that rolls the costs of home renovation projects into a single mortgage and offers more flexibility than a government loan. Conventional Renovation mortgages can cover larger, luxury upgrades, such as creating a high-end bathroom or kitchen with decorative tilework or adding a sparkling backyard pool. The maximum home repair amount is 75% of the home’s post-construction appraised value.

More Benefits of Renovation Loans and Remodeling

- Expand Your Home Search. Prospective homebuyers may have a broader range of properties to choose from, including fixer-uppers, knowing that they could finance custom home upgrades or needed repairs with a Renovation loan.

- Save on Upfront Costs. Home renovation projects can be costly. Funding home remodeling projects with your mortgage could help keep you from tapping into your personal savings and avoid hefty upfront repair costs.

- Grow Your Home Value. Renovation loans are intended to increase the value of your home, which may result in a smart, long-term investment and the potential to build more equity.

- Personalize Your Dream Home. Renovation loans offer an affordable option to help make your design visions come to life and beautify your home to fit your character.

- Enhance Comfort and Livability. Whether it’s expanding a kitchen, adding a bathroom, or creating a home office space, upgrading your home can add modern conveniences and improve your overall well-being.

If you’re looking to enhance your living spaces and potentially increase your property value, a Renovation loan could be the answer to creating the home of your dreams. To learn more about renovation financing or other mortgages, contact your local Supreme Lending branch today.

Related Articles:

by SupremeLending | Mar 15, 2024

When considering buying a home, it’s highly recommended that the first step in your homeownership journey is to work with a lender to get pre-qualified or pre-approved for a mortgage. While the two terms sound similar and both help give buyers an understanding of how much they may qualify for a loan, there are distinctions between getting a mortgage pre-qualification and pre-approval. Let’s dive into the differences between these crucial first steps and benefits of each in your homebuying experience.

Mortgage Pre-Qualification: A Preliminary Evaluation

Pre-qualification is an early step in the homebuying and mortgage process. It offers buyers and lenders alike a high-level snapshot of a borrower’s finances and potential buying power. When getting pre-qualified, lenders will typically collect basic financial information provided by the buyer, including income, debts, assets, and any amount of savings or cash they may have available for a down payment. It’s a valuable starting point, giving you an idea of your budget before you start house hunting.

During the pre-qualification process, borrowers may be able to opt for a soft pull credit inquiry. This means your information would remain confidential, with no impact on your credit score and avoids unwanted credit solicitations and third-party trigger lead calls. Ask your loan officer about your credit reporting options.

While a mortgage pre-qualification is less detailed than a pre-approval, this step can be quicker and involves less documents to help busy homebuyers hit the ground running and start their home search. A pre-qualification letter can also show sellers your interest in buying a home and that you can afford an estimated mortgage.

Mortgage Pre-Approval: A Deeper Dive

A mortgage pre-approval takes a more detailed approach and provides an even clearer, more accurate picture of a borrower’s finances and capacity for a mortgage. This is because the loan estimate is based on validated details.

In this step, prospective homebuyers will need to provide their lender with thorough documentation of their financial history for verification, including records like pay stubs, tax returns, and bank statements. Lenders will also run the borrower’s credit score and verification of employment if applicable.

Once pre-approved, the borrower will receive the estimated loan amount they may qualify for based on the verified information—verified being the key differentiator between a pre-approval and a pre-qualification. A pre-approval also gives you, the buyer, a more competitive edge because it demonstrates to sellers that you’re serious and eager to buy a home.

Other Reasons to Get Pre-Qualified or Pre-Approved

- Determine Affordability. It gives you an idea of how much you can afford based on your credit, income, debt, and potential down payment funds. This will help guide your home search within your budget.

- Understand Monthly Payments. With the estimated loan amount you can qualify for, you can get a breakdown of your monthly principal, interest, taxes, and insurance costs to help set expectations for planning your mortgage.

- Find the Right Loan Program. Evaluating your financial details and knowing how much you can qualify for can also help you determine the loan type best fit for your needs and if you could benefit from programs such as first-time homebuyer or down payment assistance.

- Strengthen Your Offer. As mentioned, having a pre-qualification or pre-approval can show sellers you’re a credible buyer and strengthen your offer on a home, which is especially helpful in a competitive market.

- Save Time. Being prepared in advance with a pre-qualification or pre-approval helps identify and avoid any potential roadblocks that could arise during the mortgage process, setting you up for a smooth closing.

In conclusion, getting a mortgage pre-qualification or pre-approval offers invaluable knowledge and opportunities in your homebuying journey. Ready to take the first step? Our Supreme Lending loan officers are ready to serve you! Contact your local branch today.

by SupremeLending | Mar 13, 2024

The decision to refinance* your mortgage is a strategic move that can have a profound impact on your financial well-being. There are several types of situations when refinancing might provide specific benefits and unlock potential savings. It’s important that homeowners have a clear idea of the possible outcomes when considering a refinance. Let’s dive into a few of the most common reasons people may refinance, some of which may apply to your situation.

Getting a More Favorable Mortgage Rate

A key reason that homeowners refinance is to get a more favorable mortgage interest rate. This can be done by either securing a lower interest rate than your current mortgage or by switching from an adjustable-rate mortgage (ARM) to a fixed-rate loan. In both cases, this may lead to significant savings over the life of the loan and may even reduce the monthly mortgage payments.

When mortgage interest rates drop lower than your current loan, it’s important to note that there are several additional considerations to be aware of, including fees and upfront costs associated with refinancing as well as the amount of time left on your current loan. Working with a trusted lender that provides personalized, transparent refinancing details and costs will help you make an informed decision for your mortgage needs.

Changing the Terms of Your Loan

Another common reason people refinance is to change the terms of their loan. This may involve extending the length of the loan to lower monthly payments or shortening the loan term to pay off the mortgage quicker. Refinancing to a shorter-term loan may increase your monthly mortgage payment, so it’s important to consider your budget before making this decision.

Switching Loan Type

Some homeowners may refinance to opt for another loan type, for example moving from an ARM to a fixed-rate mortgage. Interest rates—and subsequently monthly mortgage payments—for an ARM can increase or decrease based on market conditions, so borrowers may be more comfortable switching to a fixed-rate mortgage that has a steady interest rate and monthly payment that won’t change.

Another scenario could be borrowers wanting to change from a government loan, such as FHA or VA, to a Conventional mortgage. This could be an effective way to save on some loan costs by removing required fees typically associated with government loans.

Removing a Co-Signer

If you required a co-signer to qualify for a mortgage, you may be able to remove them from the loan by refinancing after improving your eligibility to qualify for a loan by yourself. Not only does this free up the co-signer from their financial obligation, but it may also help you qualify for a lower interest rate on your loan, especially if your credit score improves when the co-signer is removed. This could lead to more favorable loan terms. Homeowners may also want to remove a co-signer in the event of a divorce resulting in one spouse assuming sole ownership of the home and full responsibility for the mortgage.

Removing Private Mortgage Insurance or Mortgage Insurance Premium

For those who put down less than 20% down payment for a home, a common requirement is carrying private mortgage insurance or PMI. This protects the lender in case the borrower defaults on the loan, but it also means an additional monthly cost that can add up over time.

With Conventional mortgages, you don’t have to always refinance to remove PMI. It can be removed after you’ve reached a certain equity threshold in the home—usually 20%. However, some mortgage programs, like FHA loans, require a Mortgage Insurance Premium (MIP) for the life of the loan. An FHA borrower would need to refinance to a Conventional mortgage to remove the MIP cost.

Cashing Out Equity

Finally, another popular way homeowners utilize refinancing is to cash out the equity that’s built up in the home. If you refinance an amount greater than what you owe on your home, you can receive the difference in a cash payment to be used as you wish. For example, you may use this cash to fund home improvements, pay off high-interest debts, or for other large expenses. How you use the cash is up to you.

It’s important to remember that cashing out equity will increase the amount you owe on your home and may also lead to a higher interest rate—factors that should not be overlooked.

As you can see, there are a variety of reasons why homeowners may choose to refinance their mortgage. It’s important to carefully consider your individual circumstances and financial goals before making a decision, as refinancing may not be right for everyone.

For more information on reasons to refinance, or to learn more about any of our mortgage programs and services, reach out to your local Supreme Lending team or contact us today.

*By refinancing an existing loan, total finance charges may be higher over the life of the loan.

by SupremeLending | Mar 1, 2024

The men and women who have served in America’s Armed Forces have sacrificed so much to protect our freedom and communities, including time away from their families. There’s no profession more deserving of having a home to call their own. Supreme Lending is honored to provide opportunities to help Veterans and active military personnel achieve their dreams of homeownership through affordable mortgage options, including VA loans that can offer 100% financing. Let’s dive into the benefits and eligibility of VA loan programs.

Guaranteed by the U.S. Department of Veterans Affairs, VA loans are designed to help those who have served in the military and their eligible surviving spouses obtain homeownership with more flexible and favorable terms.

VA Loan Benefits

Two of the biggest benefits of VA loans are the no down payment or mortgage insurance premium requirements—making homeownership more accessible for those who may not qualify for a traditional loan. Other unique VA loan benefits and features include:

- Lower origination fees, appraisal fees, and closing costs.

- Purchase and refinance for primary homes.

- No prepayment penalties.

- Fixed- and adjustable-rate loan options available.

- Variety of eligible property types (single-family, townhomes, VA-approved condos, etc.).

- Available for qualified first-time and repeat homebuyers.

- 580 minimum credit score; 620 minimum credit score for loan amounts more than $ 766,550.

- At least 41% Debt-to-Income (DTI) ratio.

- VA non-allowable fees can be paid by seller, up to 4% of the loan amount.

- Two year waiting period after foreclosure or bankruptcy after discharged.

- Some states may offer additional options for extra affordability.

VA Loan Eligibility

A requirement of VA loans is that the homeowner lives in the home as their primary residence. A valid Certificate of Eligibility (COE) must be presented at the time of application, which includes military eligibility such as length of service or service commitment, duty status, and character of service.

VA Funding Fee

While there is no down payment requirement, VA loans do require a one-time funding fee to cover administrative or processing costs. The fee is 2.15% for first-time use of the program with zero down payment, still much lower than a traditional down payment! Additionally, the funding fee decreases to 1.5% with 5% or more down payment and to 1.25% with more than 10% down payment.

VA Loan Refinancing

Veterans Affairs also offers options for refinancing. A VA streamline refinance, also known as an Interest Rate Reduction Refinance Loan (IRRRL), could be a great option for military homeowners looking to potentially reduce their interest rate and monthly payments of a current VA loan. A VA cash-out refinance allows borrowers to leverage the equity they’ve built in their home and could help homeowners fund renovations or other large expenses.

For more information on VA loans and other mortgage options, reach out to your local Supreme Lending Loan Officer or contact us today.